This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

From sifting through investor presentations and corporate filings to listening to earnings calls and watching interviews, getting a firm gauge on an investment often requires a lot of work.

One thing that I like to do is analyze 13F filings. These are forms filed by investment firms managing over $100 million in stocks. One of the more high-profile hedge funds is Ken Griffin's Citadel. Last quarter, Citadel reduced its stake in Nvidia (NASDAQ: NVDA) by 79% -- dumping 9,282,018 shares. In addition, the firm increased its position by 1,140% in Palantir Technologies (NYSE: PLTR), scooping up 5,222,682 shares.

Let's dig into what may have compelled Griffin and his portfolio managers to sell Nvidia and buy Palantir. Moreover, I'll explore what catalysts could help fuel even more growth for Palantir -- and why now could be a great time to follow Griffin's lead.

Why sell Nvidia right now?

On the surface, selling Nvidia stock might look like a questionable move. After all, isn't artificial intelligence (AI) the next big thing?

Well, even if AI ends up being the generational opportunity it's being touted to be, that doesn't mean a whole lot at face value. There are many components to the foundations of AI, and Nvidia's expertise in the development of advanced chipsets called graphics processing units (GPU) is just one of many building blocks supporting artificial intelligence.

The biggest bear narrative surrounding Nvidia stems from rising competition. At present, products developed by Advanced Micro Devices and Intel are the most obvious alternatives to Nvidia. However, I see a bigger risk in the competitive landscape.

Namely, Nvidia's big tech cohorts including Tesla, Meta Platforms, Microsoft, and Amazon are all investing heavily into their own hardware development. Considering that many of these companies are Nvidia's own customers, I'm wary that the company's current growth trajectory is sustainable in the long run.

When more GPUs come to market, there is a good chance this technology will be viewed as somewhat commoditised. Such a dynamic will likely lead to lower prices for Nvidia, which will subsequently bring decelerating revenue, margins, and profits.

All told, I don't really blame Griffin for selling such a large portion of his Nvidia position. Despite the company's success so far, its future prospects look potentially questionable.

Why buy Palantir right now?

In a different area of the AI landscape sits enterprise software company Palantir. It offers four data analytics platforms called Foundry, Gotham, Apollo, and AIP. The company's software is used across a host of use cases throughout the U.S. military and private sector.

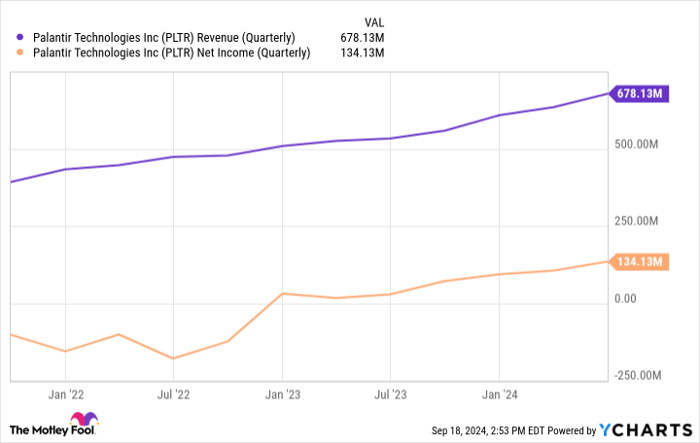

PLTR Revenue (Quarterly) data by YCharts

Investors can see that over the last couple of years, Palantir's revenue accelerated on the backdrop of a bullish AI narrative. More importantly, the company's operating leverage has improved dramatically in the form of margin expansion and consistent profitability.

Earlier this month, Palantir also achieved the notable milestone of inclusion in the S&P 500.

Should you buy Palantir stock right now?

I can't say for certain why Griffin increased his stake in Palantir so much last quarter, but I do find the timing interesting for one particular reason. Palantir has been eligible for the S&P 500 before but was not initially chosen. Perhaps some thought Palantir's newfound growth was purely an extension of demand for AI software and would not be sustainable in the long run.

Whatever the case, I think those who have followed Palantir for a long time understood that the company's long-run prospects looked solid -- regardless of the current AI narrative. Bearing that in mind, it was reasonable to think that the company would be included in the S&P 500 eventually.

This leads me to a broader point. Now that Palantir is in the S&P 500, there is a good chance more investment banks and research analysts will begin following the company more closely. In turn, this could lead to an increase in institutional investors buying the stock. Over time, this could strengthen Palantir's brand and perception in the investment community and bring the stock to even higher prices.

I think there is a good chance Palantir will witness a rise in institutional ownership. The company is quickly emerging as a force in the AI software arena, and has even attracted the likes of Microsoft and Oracle -- two relationships that I think will bring even further growth to the company.

I very much see even better days ahead for Palantir, and think now is a great time to buy shares. With so many catalysts fueling the company's upside, I see Griffin swapping Nvidia for Palantir as a particularly savvy move.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.