Image source: Getty Images

"I have watched Warren for a long time. He sits around reading and thinking most of the time. Every once in a while he talks on the phone. Part of the Berkshire secret is when there is nothing to do, Warren is very good at doing nothing."

Charlie Munger: Berkshire Hathaway Annual Shareholder Meeting – 5 May 2018

In 2013, Victor Haghani hosted a TED talk titled, "Where are all the billionaires and why should we care?" In it, he put forward a simple but interesting notion: Over the long term, the savings of a typical family do not grow as much as they should.

To support this assertion, Victor did a backtest to show that there should be far more billionaires in America today than there are, given the number of millionaires in 1900 and the stellar performance of the stock market over the last century.

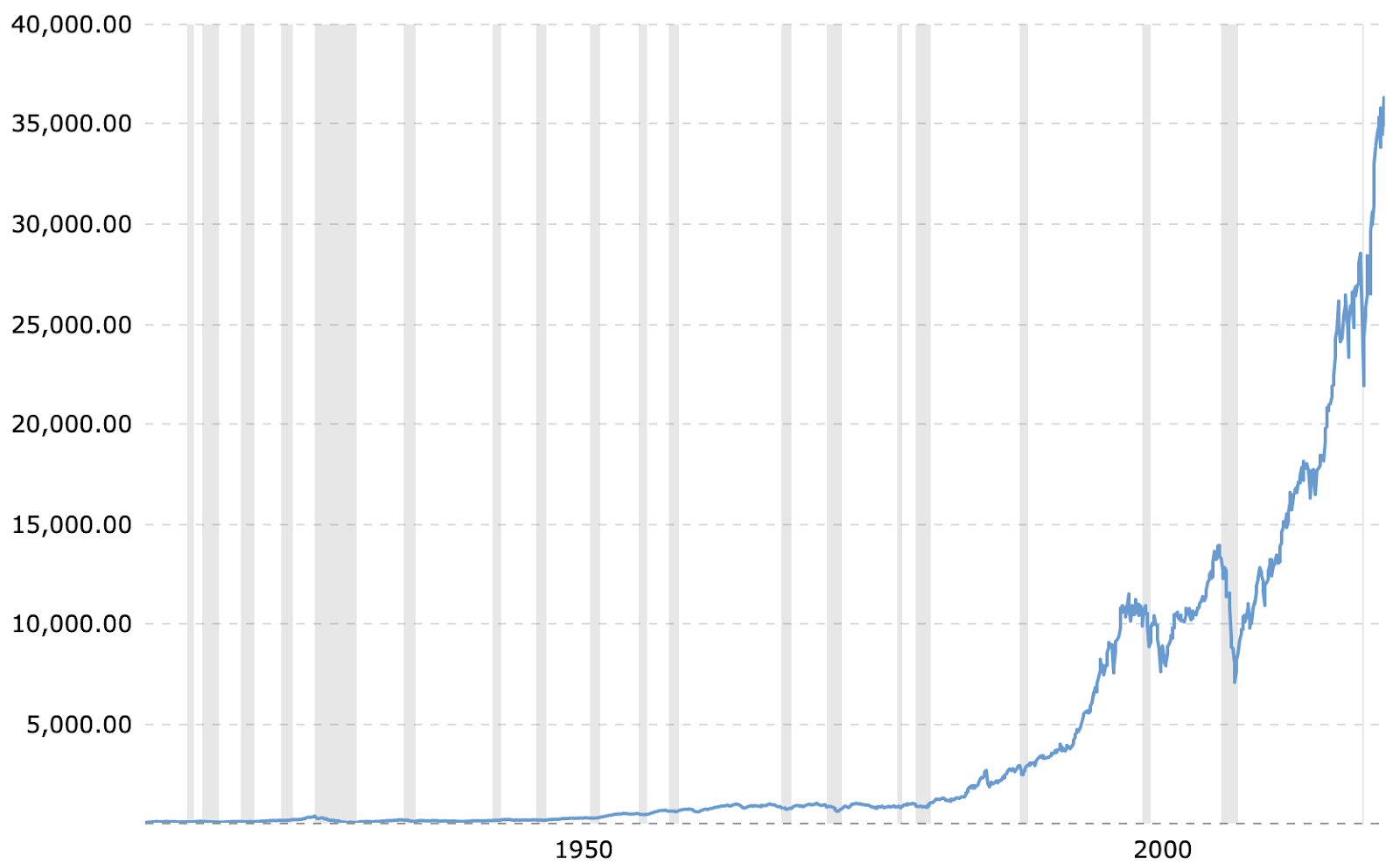

The Puzzle Of The Missing Billionaires

The US stock market, measured by the total market index, grew at a CAGR of 9.91% between 1900-2023.

Therefore US$1 million invested in passive US stocks in 1900 would have grown to roughly US$112 billion by 2023 in nominal terms – and this takes into account market crashes (denoted by the shaded areas) caused by the Great Depression, World War 2, the Cold War, Dot Com bubble, the Financial Crisis in 2008, COVID-19 and many more in between.

Source: Microtrends data

Historical data shows there were approximately 4,000 millionaires in the US in 1900. Given the net average family expansion over time, each one of those millionaires would have approximately 30 families living today.

Therefore, in nominal terms, those 30 families today should be sharing ~US$112 billion among themselves, which translates to a tidy US$3.7 billion per family.

In aggregate, the 4,000 millionaires at the turn of the twentieth century mean the US alone should have close to 120,000 billionaire families today with a combined net worth of c.US$446 trillion if their investments matched the returns of a passive investment in the US stock market.

But where are we now?

According to Wealth-X's 2022 Billionaire Census Report, there were only 955 billionaires in the US with a combined net worth of US$5.5 trillion.

The question therefore is, what became of all the other 119 000 billionaires?

The Curse Of Cognitive Biases

Humans hate being average. We do not like to see ourselves as average in anything we do. Try to survey people if they are bad, average or good drivers. Everyone believes they are either exceptional or at the very least, above average.

Psychologists have studied the human psyche and found that people tend to overestimate their abilities and the value of the information they supposedly have. Whilst these cognitive biases make us dynamic and responsive to a lot of situations in life, they unfortunately make us sitting ducks on the stock exchange, as they easily induce an inclination for action.

In other words, when it comes to investing, we find it almost impossible to sit and do nothing like Warren Buffett.

Extensive research has been conducted to quantify the cost of these inherent cognitive biases among investors.

One is to calculate the gap between what is referred to as Fund Returns and Investor Returns.

Fund Returns are the returns an investor would earn if they were to invest a dollar into any fund and just keep it there over a given period. On the other hand, Investor Returns are the weighted average returns that investors earn in any fund. They are calculated by looking at the cash flows in and out of the fund and measuring the actual weighted average Internal Rate of Return (IRR) of those cash flows.

In other words, fund returns tell you how well the fund performed and investor returns tell you how well the investors in those funds performed. One would think that these two would yield similar results but not so fast!

The results are both interesting and profound: Over the long term, the difference between Fund Returns and Investor Returns is 3% p.a; in other words, on average, investors earn 3% p.a. less than what they ought to. This is because investors tend to invest in funds after they have performed well and pull out of funds after they have performed badly. This results in investors essentially buying high and selling low.

Hyperactive investors lose much more than the 3% whereas less active investors lose much less.

Do Dead People Make Better Investors?

A study by the University of California Berkeley analysed the trading records for over 66,000 accounts in the US and found that investors who trade frequently, on average, underperform the market by up to 6.5% per annum.

Active trading is hazardous to your wealth!

In synthesising the results, the research concluded that in addition to consumption and taxes, there are two other factors for investor's relative underperformance:

- Frictional costs from active trading include transaction costs, commissions, bid/offer spreads and inefficient capital gains taxes due to heavy turnover. Active investors lose about 1% – 2% from frictional costs;

- Behavioural costs refer to self-inflicted costs from ways investors manage their money such as chasing performance, timing the market and selling at the most inopportune time. These costs, on average, reduce investor returns by 3% p.a.

So, do dead people make better investors? With inactivity and a lack of cognitive bias working in their favour, they are!

Research by Fidelity Investment Inc between 2003 and 2013 on its investor accounts concluded that portfolios belonging to people who either died or have forgotten about them tend to outperform those who are active.

While investors delight in quoting Warren Buffet, one subtle fact that is rarely mentioned is that although he started investing when he was 11 years old, it took him 44 years until the age of 55 years for his net worth to reach US$1 billion.

But only another 36 years to grow it from US$1 billion to the current US$114 billion.

If he had started investing at the age of 30, achieved the same stellar returns of 22% per annum and stopped at the retirement age of 60 years, his net worth would be around US$12 million only.

We can therefore conclude that his extraordinary returns were a combination of investment talent and patience – the ability to do nothing over a long period.

Foolish Takeaway

Time, patience and the ability to do nothing are the investor's greatest friends.

Our goal at the Motley Fool is to help you uncover great businesses worth investing in, but you have a part to play. If investors can capture the returns they ought to get, we will see a lot more smarter, happier and richer members.

But then again, as the thought experiment showed, investors only get a fraction of the returns due to them due to self-inflicted wounds of over-trading.

Ultimately, if you want to be an above average investor, it pays to play dead. Keep your investment costs low, diversify, and most importantly, manage your behaviour.

"The biggest thing about making money is time," Warren Buffett says. "You don't have to be particularly smart, you just have to be patient."