Australians born in the 1970s or later who have chosen lifecycle superannuation products have achieved the best annual rates of return over the past decade, according to a new report.

The KPMG report compared the median annual return of the traditional single-diversified MySuper Growth fund with the returns of different age groups typical of lifecycle superannuation accounts.

If you have a lifecycle superannuation account, your fund manager will automatically arrange your asset allocations in an age-appropriate way as time goes on.

The moneysmart.gov.au website explains: "With this option, your fund will typically move your money from growth investments when you're young to more conservative investments when you're older."

Single diversified MySuper funds are low-fee default funds selected by employers if an employee does not nominate a preferred fund.

Better returns for those born in the '70s or later

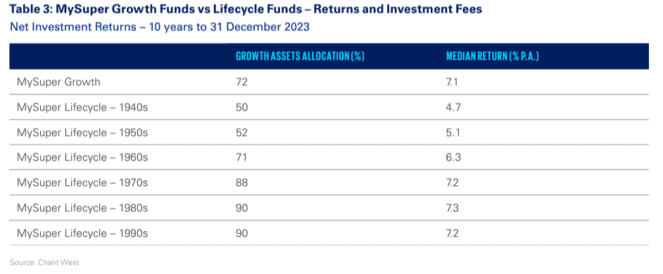

The following table published in the KPMG report uses Chant West data showing net investment returns per annum over the 10 years to 31 December 2023.

Source: Super Insights 2024

As you can see, lifecycle products suited to those born in the 1970s or later performed better. They had higher median returns per annum at either 7.2% or 7.3%.

KPMG says these higher returns reflected these lifecycle products containing a higher asset allocation in growth investments. This is because account holders were younger.

Growth investments typically include ASX shares and international equities.

Older account holders received lower median returns. They ranged from 4.7% among those born in the 1940s to 5.1% for those born in the 1950s and 6.3% for those born in the 1960s.

The returns were lower because the account holders were older and closer to retirement.

Therefore, their lifecycle funds allocated more of their money to conservative or defensive assets, such as cash and bonds, to try to achieve more capital preservation.

KPMG commented:

The older lifestyle cohorts missed out on some of the performance as they reduced risk over a period where there were generally strong returns, although they did have greater downside protection in the Covid-induced downturn in 2020 – important if they needed access to their super at that time or soon after.

Your choice of superannuation fund REALLY matters

The importance of choosing your superannuation fund carefully was apparent in the data.

Many Australians do not understand that some retail superannuation funds routinely fail to beat the market's annual benchmark returns (i.e., those of indexes like the S&P/ASX 200 Index (ASX: XJO)).

This means many super account holders pay hefty management fees in the belief they are benefitting from their fund's superior stock-picking services when, in fact, many funds fail to outdo or match benchmark returns. And once fees are paid, account holders' returns are reduced even further.

KPMG commented that the superior 10-year returns of the 1970s, 1980s, and 1990s lifecycle products barely exceeded the single-option MySuper Growth Fund.

The 10-year period saw relatively strong returns from growth assets so we would expect the younger lifecycle portfolios with higher growth assets to do much better, but they were only slightly ahead of the median single option MySuper Growth fund.

This was due to the underlying assets of these lifecycle products (mainly from retail funds) not performing as well as the underlying assets of the single option MySuper products.

Compare the performance of your current super fund

Retail funds are usually run by banks or investment firms. The Federal Government provides a comparison tool so you can compare your current super fund's performance against others.

This tool is designed to help you select a superannuation fund, with funds forced to disclose their returns.

At the time of writing, HostPlus MySuper is the top-performing fund among MySuper products with balances over $50,000. It has a 7.96% average annual return net of fees over a 9-year investment period.

The worst performer was returning 5.25%, with the Federal Government rating it 'underperforming'.

KPMG noted that lifecycle superannuation asset allocations today were different from those in the original models dating back to 2014, "some of which were far more conservative at older ages".

Superannuation outflows grow amid wave of retiring boomers

As we recently reported, new figures from the Australian Prudential Regulation Authority (APRA) out this week showed greater growth in superannuation outflows than inflows over the year to 31 March 2024.

This was largely due to more benefit payments going out as more baby boomers entered retirement.

Baby Boomers were born between 1945 and 1964, making the youngest Aussies in this cohort 60 years of age this year.

This means every baby boomer has now reached preservation age. That's the age at which we can all begin accessing our superannuation savings.

The data shows $112.9 billion was paid out, up 18.1% annually. Inflows totalled $177 billion, up 11.3%.

APRA said the increased outflows were directly linked to more lump sum and pension payments:

This increase was the result of lump sum payments rising by 18.4 per cent to $63.0 billion and pension payments increasing by 17.7 per cent to $49.8 billion.