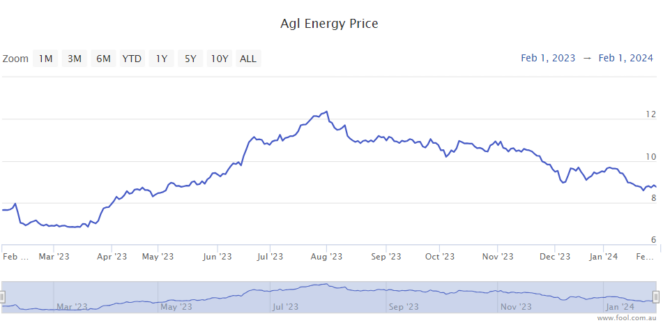

The AGL Energy Ltd (ASX: AGL) share price has seen most of its gains now reversed. It's up 12% in the last year, but has fallen 30% from 1 August 2023.

It's a tricky situation for investors because the short-term profitability of the business looks very strong, which seemed to be largely why the AGL share price went up so much in the six months after February 2023.

AGL is expecting to release its FY24 half-year result on 8 February 2024. Should investors buy before then?

Strong profitability expected in FY24

AGL has provided guidance that suggests its underlying net profit after tax (NPAT) could at least double in FY24.

FY24 underlying earnings before interest, tax, depreciation and amortisation (EBITDA) is expected to be between $1.875 billion to $2.175 billion, while underlying NPAT could be between $580 million to $780 million.

There were a few reasons why the company gave such strong guidance.

AGL pointed to "sustained periods of higher wholesale electricity pricing, reflected in pricing outcomes and reset through contract positions."

The company also noted it's expecting "improved plant availability and flexibility of the asset fleet, including the commencement of operations of the Torrens Island and Broken Hill batteries, and the non-recurrence of forced outages and market volatility impacts from July 2022 of around (pre-tax) $130 million."

If we look at the current AGL market capitalisation of $5.83 billion, according to the ASX, it's valued at between 7 times to 10 times estimated earnings. This could also mean a stronger dividend from AGL if the board are feeling confident.

What's going wrong for the AGL share price?

However, there's also the fact that energy prices have reduced. This reduces the potential revenue generation in the future.

As the Australian Energy Regulator recently said on 31 January 2024:

The Australian Energy Regulator's (AER) latest Wholesale Markets Quarterly Report reveals that average annual wholesale electricity prices in the National Electricity Market (NEM) fell by between 44% and 64% and average annual east coast gas market spot prices fell by 43% in 2023.

This was attributed to milder weather conditions, lower fuel costs, fewer coal supply issues and an increase in cheap wind and solar supply.

The report also shows wholesale electricity prices during the October to December 2023 quarter fell in NSW, VIC and SA but increased in QLD and TAS compared to the previous quarter, with gas prices on the east coast spot market increasing slightly compared to the previous quarter.

Both electricity and gas prices during the quarter remained well below the record prices of 2022 and were now closer to longer term annual averages. Once retailers' wholesale costs adjust to the lower prices going forward, prices faced by consumers should reflect these lower costs.

Electricity demand fell compared to the previous quarter between 9% and 19% in all regions except QLD, where hot and humid periods drove increased use of air conditioning units.

It's tough to judge AGL from here – can electricity demand rise again, particularly if temperatures rise? That could significantly help profitability. The strength in the first half of last year surprised investors and this weakness has also surprised.

Is the AGL share price a buy?

It's certainly looking like an unloved stock again. I think it could be an underrated business in the current situation, and perhaps overly sold. It's possible a bout of warmer weather could turn around electricity demand.

I don't think it's going to be the next one I buy, but I'm optimistic that FY24 could be strong. Energy prices could swing upwards again, but it's also facing a lot of competition from rooftop solar.

It could be one watch this ASX reporting season.