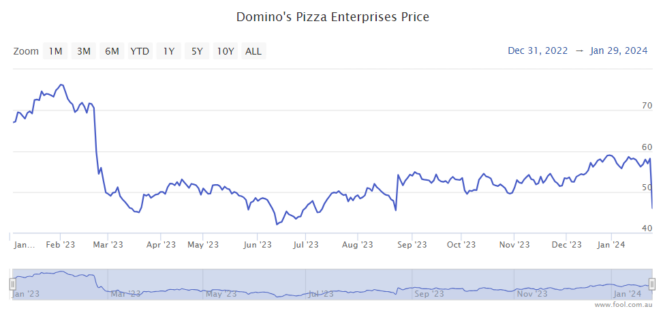

The Domino's Pizza Enterprises Ltd (ASX: DMP) share price has plunged 30% compared to a year ago. Is this a great opportunity to invest in the stock, or is there worse to come?

It's impossible to say what's going to happen next without my crystal ball, which isn't working at the moment. The Domino's share price could fall further and/or the upcoming results could show a deterioration of profitability. But, things could also get better.

The recent business update triggered the Domino's share price decline. Domino's reported an 11% rise in ANZ network sales in the FY24 first half compared to the FY23 second half, while Asian network sales fell 1%.

Domino's blamed Japanese network sales going backwards as a key negative factor, referring to the number of corporate stores in that market. Net profit before tax is expected to be between $87 million to $90 million, which is below HY23, but above the FY23 second half.

It said while franchisee partners in ANZ and Europe are improving average unit economics, there is more work to do. Improvements are required in the FY24 second half to grow order volumes. Domino's advised any previous guidance for its FY24 performance is "no longer in effect".

Is the Domino's share price an opportunity?

The broker UBS Is pessimistic about the situation and has a sell rating on the business because of a few reasons.

First, it's another announcement that was below expectations, which isn't a good sign.

Second, there are concerns that ANZ's improvement is "less able" to be translated into other high store growth markets, particularly Asia and France, though Germany's performance is "pleasing".

The third reason is that franchisee profitability is improving but not as quickly as expected, "which places risk on the rate of store growth (or the long-term Domino's EBIT margins)".

Finally, UBS also referred to "elevated valuation multiples".

Based on Domino's share price, UBS thinks the company is valued at 28 times FY24's estimated earnings.

But, it does have a price target of $42, implying a possible small rise over the next 12 months.

Any positives?

UBS isn't loving the short-term outlook for the company, but it is still expecting the business to stage a profit recovery in the long term.

The broker is expecting Domino's to report an FY24 EBIT margin of 9%. But, this could rise to 10.7% in FY25, 12.2% in FY26, 13.2% in FY27 and 13.8% in FY28.

Domino's is also expected by UBS to see growing revenue in each of these financial years. Earnings per share (EPS) could be $1.43 in FY24, $1.75 in FY25 and $2.10 in FY26.

This would put the Domino's share price at 19 times FY26's estimated earnings. Of course, these numbers are just forecasts. Forecasts can be wrong – the profit could be worse (or better) than expected.

Store numbers may not grow as quickly as investors (or the company) were previously thinking, but the company still has compelling intentions. The strength in the German market is exciting because of what a large market that is.

With the Domino's share price now much lower, I think it's at a much more appealing price which could enable it to deliver outperformance from here. While it's unlikely to be an uneventful journey from here, I think Domino's shares could deliver outperformance in the next three to five years, particularly if the business can improve profit margins.