We all want to find a bargain on the ASX share market. A number of S&P/ASX 200 Index (ASX: XJO) shares have been sold off in recent months which could be cheap opportunities. I'm going to look at two of them in this article.

Just because something has fallen hard doesn't mean that it's necessarily a good buy. However, we might be able to find a good idea if we think with a contrarian mindset.

With some business conditions, like discretionary spending or commodity prices, we often see a cycle. When conditions go bad, share prices are likely to fall. It could be an opportunity to invest while the market is negative or fearful and benefit when conditions normalise, or even boom.

On a three-year or four-year view, I think both of these ASX 200 shares are opportunities for a strong rebound. The next 12 months (or so) could be very volatile or even worse for them, but I think these are contrarian ideas that could do well.

Charter Hall Long WALE REIT (ASX: CLW)

This is a real estate investment trust (REIT) that invests in a variety of property sectors including hospitality, service stations, retail, industrial and logistics, office, social infrastructure and agri-logistics.

It has a long portfolio weighted average lease expiry (WALE) of 11.2 years, with 99% of tenants being blue chip, which includes government, ASX-listed, multinational and national tenants.

Around half of the ASX 200 share's leases are linked to CPI with a 7.1% weighted average increase of CPI-linked leases in FY23. The other half of leases have an average fixed increase of 3.1%.

Over the past six months, the Charter Hall Long WALE REIT share price has fallen around 25% and it's down close to 40% from April 2022. That's despite the business having quality properties, seeing good income growth and still paying good distributions.

It's expecting to pay a distribution per unit of 26 cents in FY24, which would be a distribution yield of 7.9%.

Charter Hall Long WALE REIT said that its net tangible assets (NTA) was $5.63. If the business sold all of its properties it may get less than $5.63 per unit, but the share price discount is at around 40%, so this gives us a good margin of safety.

Credit Corp Group Limited (ASX: CCP)

Credit Corp is a debt collector in the US and Australia and also has a lending division in Australia. I recently covered the company's decline, with the company down 40% from mid-September.

The collection environment is worsening in the US for the ASX 200 share, which is going to hit profit in FY24. That's why it's including an impairment in its upcoming result.

Of course, it's understandable that investors are worried about the company seeing less successful collections. It reduces profit in the shorter term, hurts assumptions and could mean that things are getting worse.

From my point of view, I don't see a catalyst in the shorter-term foreseeable future that will improve economic conditions for the business. Interest rates in the US and Australia may stay higher for longer than what people were hoping for, making it trickier for Credit Corp.

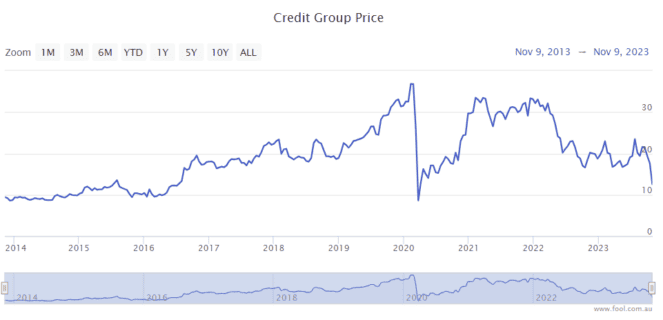

I think the last decade of the Credit Corp share price (on the chart below) is quite demonstrative that the business was steadily growing until the COVID-19 crash hit. The Credit Corp share price is almost back to those lows seen in 2020. I'm definitely not expecting a quick recovery – a recovery could take years.

Which ASX 200 share is better value?

I believe that both ASX 200 shares could be undervalued on a longer-term view. Charter Hall Long WALE REIT is the lower-risk option in my opinion as interest rates are not likely to go much higher. But its performance is likely linked to rental growth (which probably won't be that fast) as well as interest rate cuts down the line, eventually.

Credit Corp shares may suffer further falls from here, but I believe it has a stronger chance of delivering bigger returns over the next several years because of its ability to expand and recover when conditions improve again.