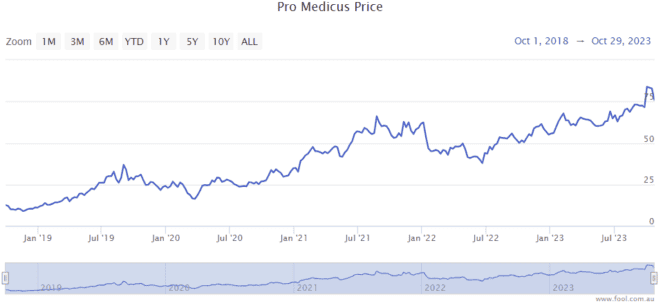

Pro Medicus Ltd (ASX: PME) shares have done incredibly well over the short and longer term.

They have risen by 40% in 2023 and are up a hefty 630% over the last five years, as we can see in the chart below.

Shareholders have certainly done very well with this ASX healthcare share. But after such a strong run, investors may wonder whether it has performed too well.

Looking at FY23, the company generated earnings per share (EPS) of 58 cents. That means it's currently trading at 131x FY23's earnings. That's a high price/earnings (P/E) ratio in anyone's book.

Are Pro Medicus shares too expensive?

It's important to remember that the (ASX) share market is typically forward-looking. That means that what's going to happen in the future is more important than the past. So FY24 (and beyond) is more important to investors than FY23.

According to Commsec predictions, Pro Medicus is projected to make EPS of 74.5 cents in FY24 and 96.2 cents in FY25. That would put the current Pro Medicus share price at 102x FY24's estimated earnings and 79x FY25's estimated earnings.

Those are high P/E ratios, particularly when you consider that interest rates are now much higher than they were a couple of years ago. And they're expected to stay higher for longer.

However, the company is delivering strong revenue growth and is expected to keep growing revenue, and it has strong profit margins for that good revenue.

In FY23, revenue from contracts with customers increased by around 34% to $124.9 million. In FY24, Goldman Sachs' current forecast implies a possible 27.7% revenue rise to $159.5 million. Meanwhile, FY25 revenue could increase a further 28% to $205.4 million.

Strong earnings, more contracts

The business has an enormous earnings before interest and tax (EBIT) margin of 67.2%. That means just over two-thirds of new revenue is turned into EBIT. It's one of the best EBIT margins on the ASX.

With that in mind, I suspect that a lot of the $80 million extra revenue it's projected to add over the next two years will turn into EBIT. And after paying income tax, a large chunk of the EBIT will turn into net profit after tax (NPAT).

Pro Medicus is steadily adding more contracts, which boosts its long-term revenue profile. For example, a month ago, it signed an A$140 million, 10-year deal with Baylor Scott & White.

If it wins a few more sizeable contracts in the next several months, then the revenue and profit outlook will improve even further for FY24 and FY25.

The Pro Medicus share price may look expensive with the forecast earnings over the next year or two. However, its future profit growth keeps looking more positive.

I've thought that the company has seemed expensive over the years, yet it keeps doing extraordinarily well for shareholders.

Long-term growth

A lot of the company's success is coming in the United States. There are still many more US contracts it can win, and it seems to be winning a large amount of the contracts that come up for grabs.

There are plenty of other regions that Pro Medicus can expand (more) in, such as mainland Europe, the UK, Asia and so on. Being successful in other regions could boost the Pro Medicus share price further.

It's possible that Pro Medicus could diversify its earnings in the future by growing its existing offering, creating a new offering or acquiring a business for a rapid change.

The Pro Medicus share price is decided by more than just the next year or two of financial results. The long-term looks very positive, so I think a P/E ratio of more than 100 can be justified as time goes on, though the current valuation may make it hard to outperform in the shorter term.