Rising interest rates have long been a highly effective and thoroughly blunt instrument in tamping down home values in Australia.

You might think that's the case in every property market worldwide, but you'd be wrong.

The impact here is greater for two big reasons.

Firstly, three-quarters of our housing debt is on variable rates, whilst many other countries have long-term fixed-rate mortgages.

Secondly, we have the second-highest household debt in the world, behind Switzerland, at 111% of GDP.

So, when the Reserve Bank raises the cash rate, Australian mortgage holders feel a big financial whack.

Therefore, it's not surprising that the fastest increase in interest rates ever seen in Australia coincided with the steepest fall in property values in more than four decades.

With all that in mind, Australian home values have staged a remarkably strong comeback in 2023.

It's particularly curious given we're still in a rate hiking cycle (albeit pretty close to the end). On top of that, it's not just home loan repayments going up — it's everything else under the sun, too.

So, why are home values rising?

To recap, the property market went through a steep correction in 2022. This was brought on by the RBA raising rates in eight consecutive months from May to December.

We had another two rate rises in February and March, and that's when home values began to rise.

The next two rate rises in May and June did not interrupt that trajectory. We've since seen seven consecutive months of home price growth, adding up to a 5.7% lift in the national median dwelling price as of the end of September, according to the latest CoreLogic data.

So, why did home values start rising when interest rates were still on the up?

And have ASX property shares and real estate investment trusts (REITs) gone up too this year?

Image source: Getty Images

The drivers behind rising Australian home prices

We've got a perfect storm situation going on right now.

A confluence of factors is causing the strong property market turnaround.

The big one is supply.

Australia has been undersupplied for many years, and it's an issue that has taken up permanent residency in the too-hard basket for our politicians. Among the issues is strict building regulations imposed by individual local councils, which many developers say stymie development.

The pandemic exacerbated the undersupply, with recurring lockdowns delaying building for two years.

Then, once COVID-19 was over, we saw a massive global supply chain ruction as builders from all over the world competed for construction materials at the same time.

This led to delays in completing projects and significant price hikes for materials. The cost of building a home in Australia in 2022 rose at its fastest pace since the introduction of the GST in 2000.

The effect is still being felt today, with new home purchases (and rents) among the top three contributors to the 1.2% inflation growth recorded in the September quarter.

Meantime, the number of homes for sale is lower than usual. That's because many homeowners feel no motivation to move in today's difficult economy. Long-term tenure rates in many markets are also rising, with the huge cost of stamp duty thought to be a contributor to people preferring to stay put.

As a result, the supply of homes for sale is tight.

CoreLogic Research Director Tim Lawless says the markets experiencing the strongest capital gains in the September quarter — Adelaide at 4.3%, Brisbane at 3.9% and Perth at 3.6% — also have advertised stock levels that are 40% below their five-year averages.

Supply vs. demand

On top of these supply-side issues, Australia is experiencing a population surge.

The Federal Government projects a net gain of 715,000 migrants over the next two years. That sort of rapid population growth puts immediate and direct pressure on housing.

The Reserve Bank notes that low unemployment and large amounts of savings accumulated during the pandemic have enabled homeowners to weather the rise in home loan repayments to date.

And FYI, the bank reckons Australian homeowners can take another rate rise, too.

In a report released this month, the RBA said:

Most borrowers are also expected to be well placed in the event of a further increase in interest rates. The direct effect of a hypothetical 50 basis point increase in the cash rate to 4.6 per cent increases the estimated share of variable-rate owner-occupier borrowers who are unable to cover their expenses from around 5 per cent to around 7 per cent.

Of these borrowers, about 30 per cent are at risk of depleting their buffers within six months (equivalent to 2 per cent of all variable-rate owner-occupier borrowers).

Now, onto those ASX REITs and their share price movements in 2023.

Are ASX REITs going up like home values in 2023?

The short answer is no, and we'll tell you some reasons why.

First of all, let's take a look at the performance of ASX REITs.

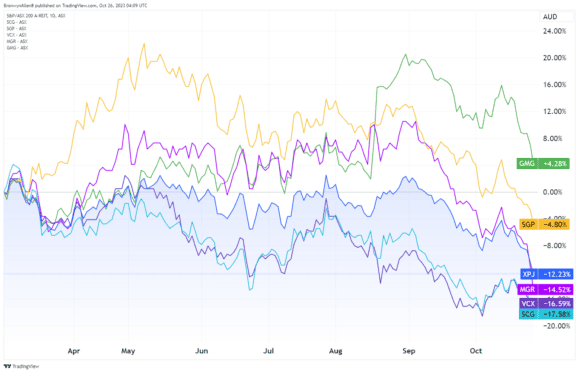

We'll do this by analysing the S&P/ASX 200 A-REIT Index (ASX: XPJ) and its movement since March, when home values started to rise.

As you can see below, ASX REIT shares are down 12.23% since March vs. property values rising 5.7%.

We've also included the five biggest ASX REITs by market capitalisation on the chart. All bar one has lost value since 1 March.

- Goodman Group (ASX: GMG) shares rose 4.28%

- Scentre Group (ASX: SCG) shares lost 17.58%

- Stockland Corporation Ltd (ASX: SGP) shares lost 4.8%

- Vicinity Centres (ASX: VCX) stock lost 16.59%

- Mirvac Group (ASX: MGR) shares lost 14.52%.

Why ASX REITs aren't moving in line with home values

The biggest reason is the bulk of ASX property shares and REITs are not exposed to residential property.

Instead, they are exposed to commercial property. This includes retail shops, office blocks, hotels, and industrial properties like warehouses and factories.

All of these different property types operate on different market cycles. They are also impacted by varying economic forces and in different ways to residential property.

For example, a sluggish economy like we have today does not change humans' need for shelter, but it does change humans' desire to start or expand businesses that use commercial property.

There are also sector-specific forces that impact commercial property.

For example, the rise in e-commerce is upping demand for warehouses and lowering demand for retail spaces. Meantime, the work-from-home trend has lowered demand for offices, and the explosion of short-stay accommodation has affected hotel patronage.

ASX REITS also tend to have global portfolios of real estate assets. That means the economic health of many countries — not just Australia — has an impact on asset valuations and rental returns.