I love finding ASX shares that look like opportunities. I prefer to find companies I could own forever, but an investment with a three to five-year timeframe could also work out well. In my opinion, Rio Tinto Ltd (ASX: RIO) shares are a stock worth watching.

I'm not saying the ASX mining share is a great buy today, but it's something that I believe could deliver investors good returns at the right time.

Rio Tinto is a leading miner in the iron ore space. Demand for iron ore can fluctuate quite significantly, largely due to China. While construction in the Asian powerhouse may not be using as much iron ore as it used to, other areas of the economy seem to be picking up the slack, such as vehicle production. The iron ore price is currently close to US$120 per tonne, which is a solid price and means the company is generating good earnings.

However, there are a couple of other reasons why I think Rio Tinto shares can be a good investment at the right price.

Image source: Getty Images

Copper

As Rio Tinto points out, copper is used in a large array of different applications such as pots and pans, water pipes, radiators in cars, as well as computers, smartphones, electronics, appliances, electric vehicles and electricity transmission. An electric vehicle uses three to four times more copper than a 'traditional' vehicle.

Another copper use is wind turbines – a 1 MW wind turbine uses three tonnes of copper.

According to Rio Tinto, global demand for copper is set to grow from 1.5% to 2.5% per year.

The business is expanding its copper exposure. It has grown its ownership of Oyu Tolgoi, a region in Mongolia, which is one of the largest known copper and gold deposits in the world. When the underground mine is complete, it will be the fourth-largest copper mine in the world.

It also has its Kennecott operations which it's looking to expand. Rio Tinto is looking to expand the Resolution copper project in the US and Winu in Western Australia. Rio Tinto also has a minority stake in the La Granja copper project in Peru.

Lithium

I also like that the business is expanding in the lithium space as well, considering the projected growth of electric vehicles and other battery usage.

According to Rio Tinto, double-digit growth in lithium demand is forecast over the next decade.

While the Jadar project may not go ahead, the Rincon project in South America has a lot of potential and it'll be interesting to see what future moves the company makes in this space.

Why I added Rio Tinto shares to the watchlist

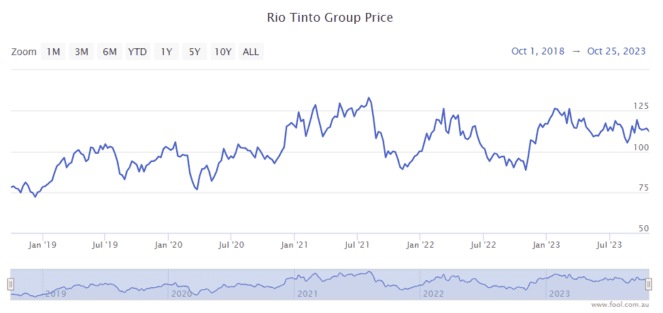

I'm certainly not an expert in mining, China or related areas like that. But, it is understandable that the Rio Tinto profit is cyclical, so the Rio Tinto share price can move cyclically as well. Just look (below) at how the share price has moved over the past five years.

When markets are fearful about commodities or China, I think it's a good time to consider Rio Tinto shares. The business is invested in commodities that are expected to see long-term demand growth because of decarbonisation, so there are long-term tailwinds.

It's not at a price yet where I'd invest, but I'm going to keep a close eye on the business.