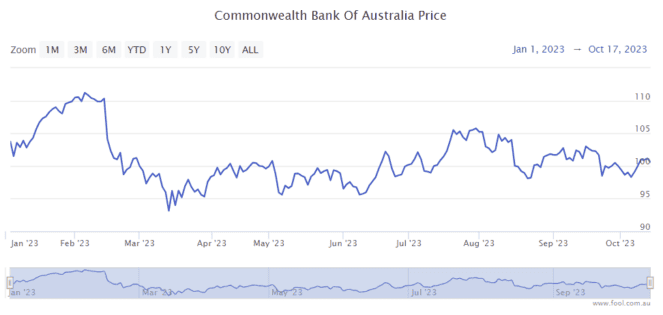

The Commonwealth Bank of Australia (ASX: CBA) share price is lower than where it was in both July 2023 and February 2023, as we can see on the chart below. Could the ASX bank share be a buy at around $100?

It's impossible to know what's going to happen next with the ASX share market.

The ASX bank share sector is particularly unpredictable at the moment because there are a number of powerful forces at play including strong levels of competition, higher interest rates and rising arrears.

Banks have to find the balance between achieving a good net interest margin (NIM) for profitability and shareholders, a low enough interest rate to keep existing borrowers and win new ones, as well as ensuring that borrowers aren't crushed by the high interest rate environment.

Bank of Queensland Ltd (ASX: BOQ) recently reported its FY23 half-year result which showed that it had seen a slight deterioration of its NIM as well as a slight reduction of its home lending loan portfolio balance.

I think the difficulties in the sector are why the share prices have been so volatile.

Image source: Getty Imgaes

Is the CBA share price a buy?

As you might expect, there are a variety of different opinions out there.

Writing on The Bull, Tony Locantro from Alto Capital called CBA a sell because it trades at a premium compared to other banks and suggested that "investors may want to lighten holdings given potential economic headwinds moving forward."

Also writing on The Bull, Tom Bleakley from BW Equities suggested that the CBA share price is a hold. He also noted that the ASX bank share trades at a premium to global banking peers, though he continues to view CBA as a "high-quality option for investors looking for banking exposure." The problem is that "generating growth may be challenging in what could be a slowing economy during the next 12 months."

According to the analyst ratings collated by Factset, there are no buy ratings for the bank, three hold ratings and 12 sell ratings.

In my opinion, CBA is one of the highest-quality banks in Australia and probably in the world. Does it deserve to trade on the premium that it does to other ASX bank shares? Perhaps.

I don't mind suffering through some volatility as an investor – and there could be a fair bit of volatility in the next 12 months – but what holds me back the most about CBA is (in my view) its lack of profit growth potential in both the short-term and the long-term.

CBA is a huge business, with a market capitalisation of $169 billion. I'm not sure its margins can become much better than they are right now, so loan growth and arrears will be key. Its loan book is already huge, so it becomes difficult to keep growing at a good pace in percentage terms.

Valuation

According to Commsec (which has third-party estimates), the CBA share price is valued at 18 times FY24's estimated earnings with a forecast grossed-up dividend yield of 6.3%.