Shares included in the S&P/ASX 200 Index (ASX: XJO) come with an assumed level of quality and respect. It is, after all, the pre-eminent benchmark for listed Australian companies.

Despite its notability, the illustrious index is not exempt from housing ineffective investments. A company's membership to the benchmark depends on its market capitalisation, trading liquidity, and presence on the ASX.

You might be surprised to learn that companies without sales ($0 in revenue) are included in the ASX 200. As such, the quality of some index constituents is questionable, to put it lightly.

Here's a look into one ASX 200 share I'm steering clear of and why.

Image source: Getty Images

Red flags galore

Tabcorp Holdings Ltd (ASX: TAH) is a company that some fund managers might consider a 'turnaround' stock. However, I believe this besieged betting house is not worth the entry price, which closed yesterday at $1.115 per share — trading flat year-to-date.

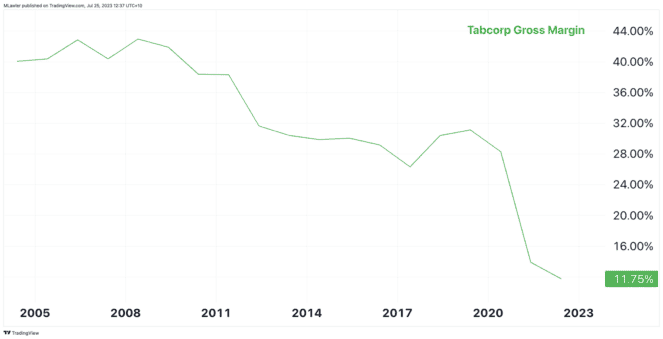

Firstly, Tabcorp's gross margins have dwindled over the past two decades. If I had to guess the cause, my finger would be pointed at increased competition from Sportsbet, Bet365, and Ladbrokes. Larger international companies, including Flutter Entertainment and Entain, back these rivals.

The declining gross margin, as shown below, suggests the sports gambling industry is highly competitive despite its regulatory barriers. Additionally, this might allude to a lack of differentiation available through Tabcorp's product offering.

Last week, I delved into the importance of a high return on capital employed (ROCE), a metric put to work by investing legends Warren Buffett and Terry Smith. In short, a ROCE above the company's cost of capital can be a much better indicator of value creation than earnings per share (EPS).

Picking stocks with a history of generating a ROCE far beyond any likely cost of capital can lead to phenomenal investments.

Now, without getting into the nitty-gritty of calculating the cost of capital, we might assume that a 'likely' cost might be between 4% to 10%. For this ASX 200 share, its recent ROCE was approximately 2%, feasibly lower than its capital cost.

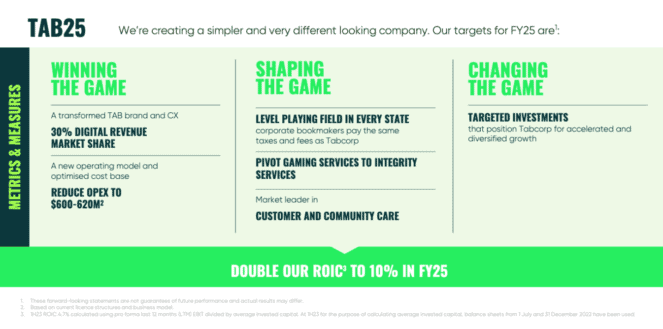

It seems Tabcorp is well aware of its less-than-ideal performance. Hence, there's a plan known as TAB25 to bring about change. Unfortunately, this looks like IBM's 2015 roadmap, which Smith included in his book Investing for Growth.

As stated by Smith, "Acquisitions, cost-cutting and share buybacks are not a particularly high-quality source of growth." Buybacks are not applicable for this ASX 200 share. However, the reduced operating expenditure and 'targeted investments' are.

This brings me to Smith's Law: you should never use an expression if its opposite is so nonsensical that you would never say it. 'Targeted investments' is a fitting example of gimmickry — were accidental investments an option?

Lost the better part of this ASX 200 share

Before June 2022, you could argue that parts of Tabcorp were 'good businesses'. That was before The Lottery Corporation (ASX: TLC) was demerged, spun off, and listed as its own ASX 200 share.

The Lottery Corp essentially holds a monopoly over lottery sales across Australia, excluding Western Australia. That is a far better proposition for a shareholder than the immensely competitive landscape of sports betting.

For this reason, I'd be much more inclined to invest in The Lott as the better ASX 200 share, before considering Tabcorp.