Every stockpicker wants to own great companies capable of outperforming the market over many years. Investors will usually evaluate shares — including those in the S&P/ASX 200 Index (ASX: XJO) — on numerous fundamentals to achieve this.

The usual suspects include the price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, margins, and earnings per share (EPS), among others. These can all help paint a picture of whether we're looking at a good company.

However, none of these measures illustrates how effective the company is at truly creating value for shareholders. Yet, it's the act of producing more capital than is consumed that predominantly generates returns over the long term.

This can be measured. It's called the return on capital employed (ROCE) — investing greats, such as Warren Buffett and Terry Smith, have been using it for decades.

Image source: Getty Images

Why is ROCE an important yardstick?

Growth is great. We all want the earnings of our portfolio companies to grow. I want to be clear, increasing EPS itself is not a negative. It is how those earnings are growing and at what cost that can create concern for shareholders.

Is a 10% earnings yield good? How about 15%? Better still, what if it were 20%?

The answer to all of those should be not enough information is provided. To determine a satisfactory return, we need to understand the cost of the return. Much like if you were to borrow money and generate a 10% return — it would be a good outcome if borrowing costs were 5%. Not so swell if they were 15%.

Using ROCE, investors can see how efficiently an ASX 200 share (or any other) has used its capital to generate profits. It also enables a more level comparison between companies with different capital structures e.g. those that use debt and those that don't.

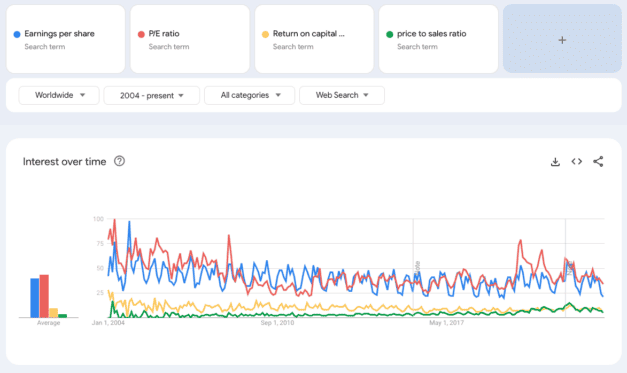

As Warren Buffett described in his 1979 annual Berkshire Hathaway letter, ROCE is the primary test of performance in managing a company. Despite this statement, the metric has played second fiddle to others, including the price-to-sales (P/S) ratio in recent years, as shown above.

Which ASX 200 shares top the list?

Struck by the notable absence of the ROCE elsewhere, I thought it would be interesting to see which ASX 200 members are excelling on this basis. After running the numbers, I concluded the below companies hold the highest ROCE currently:

| ASX-listed company | EBIT (millions) | Capital Employed (millions) | ROCE |

| Deterra Royalties Ltd (ASX: DRR) | $254.90 | $151.63 | 168% |

| Pilbara Minerals Ltd (ASX: PLS) | $1,708.80 | $1,641.10 | 104% |

| Netwealth Group Ltd (ASX: NWL) | $85.48 | $118.60 | 72% |

| Whitehaven Coal Ltd (ASX: WHC) | $3,417.20 | $5,074.70 | 67% |

| New Hope Corporation Limited (ASX: NHC) | $1,763.17 | $2,889.80 | 61% |

| BHP Group Ltd (ASX: BHP) | $58,075.20 | $113,567.70 | 51% |

| Pro Medicus Limited (ASX: PME) | $66.00 | 130.20 | 51% |

| JB Hi-Fi Limited (ASX: JBH) | $876.60 | 1,855.10 | 47% |

| TechnologyOne Ltd (ASX: TNE) | $117.34 | 268.80 | 44% |

| Lovisa Holdings Limited (ASX: LOV) | $102.02 | 237.40 | 43% |

As you can see above, ROCE is a function of earnings before interest and tax (EBIT) divided by capital employed (total assets minus total current liabilities). All of which can be found in a company's financial statements.

For transparency, one ASX 200 share ranked above Deterra Royalties but was excluded due to its EBIT being inflated by a one-off transaction.

That aside, the above list gives an insight into the most capital-efficient businesses on the ASX. The high number of resource-related companies — such as Deterra, Pilbara Minerals, Whitehaven, and New Hope — is a byproduct of strong commodity prices.

Several years of ROCE would need to be mapped out to gather a more informed view.

Putting it to work

The ROCE is not without its flaws. It is only as good as the numbers flowing into the calculation, susceptible to miscategorisation and manipulation.

Adding to this, anomalies happen. Only because I knew a company's earnings benefitted from a one-time sale did I exclude it from consideration.

That's why obtaining an all-encompassing view of a company is still helpful. Ideally, I'd calculate the ROCE for an ASX 200 share over a five to ten-year period before calling it a 'track record'.

Generally, a return on capital employed above 20% is solid.