Over the past two weeks, no other company has dominated the headlines quite as much as Nvidia Corporation (NASDAQ: NVDA). Shares in the semiconductor giant, known for its graphics processing units (GPUs), have shot up 30% following the company's quarterly results.

The prolific rise of AI-powered tools and tasks is prompting data centres to overhaul their hardware to better suit this new wave. Being a primary provider of accelerated computing hardware, Nvidia is surfing this AI tsunami.

However, at a price-to-earnings (P/E) ratio of 207, could investors be pricing in too much? Here's a brief analysis of whether I think Nvidia shares are worth the accompanying trillion-dollar price tag.

Setting the scene

The current landscape of artificial intelligence has been described as 'the next internet' and having its 'iPhone moment'. Indeed, the excitement is palpable, as the technology promises to pave the way to a more productive and creative future.

It's hard to ignore the numbers being thrown around. Grand View Research estimated the global AI market to be $207 billion last year, forecasting it to grow at a compound annual growth rate (CAGR) of 37.3% to 2030.

Likewise, Goldman Sachs analysts believe generative AI could boost global GDP by $7 trillion and provide much-needed productivity growth.

Nvidia co-founder and CEO Jensen Huang has an eye-watering figure of his own. He expects $1 trillion worth of installed infrastructure to transition to accelerated computing over the next decade as generative AI becomes the "primary workload" of data centres.

Welcome to the AI ecosystem

Clearly, the market opportunity in AI is large, based on the above, but how would Nvidia shares benefit more than other semiconductor companies? It comes down to raw power.

Both the training and running of AI are incredibly compute-intensive. The rush to develop even more sophisticated AI necessitates the processing of more data in the form of large language models (LLMs) at a faster pace.

The team at Nvidia realises this. Their solution — providing unified componentry to increase throughput and power.

Unlike its competitors, Nvidia is broadening its computational land grab by supplying the networking hardware, the central processing units (CPUs), the GPUs, and the software.

Previously, many of the world's most powerful supercomputers used a mishmash of parts from Nvidia and others such as Intel Corporation (NASDAQ: INTC) and Advanced Micro Devices Inc (NASDAQ: AMD).

By offering the full spread of hardware for accelerated computing, Nvidia can optimise the solution where others cannot, such as the use of bidirectional memory referencing between the CPU and GPU.

What this enables is 256 Nvidia Grace Hopper Superchips being seamlessly connected in a single data hall, pictured above.

Further, I believe the desire for maximum speed and efficiency among customers will drive an even stronger monopoly in data centre hardware, and Nvidia is the frontrunner.

Certainly, it becomes an uphill battle for AMD and Intel to sell CPUs if Nvidia offers an all-in-one solution.

How it becomes a moat

This leads me to what I believe is the company's moat. In my opinion, Nvidia is becoming the enterprise version of Apple. That is, build an install base through exceptional hardware; the hardware creates a high switching cost; then offer value-add software at high margins.

Nvidia's computing platform CUDA is its iOS while Nvidia's AI and Omniverse are its answer to Apple's lucrative services business.

Today, there are millions of developers are using CUDA, a programming model for GPUs. In turn, many of the most advanced computing applications are exclusive to Nvidia. The flywheel will likely attract more developers and more advanced applications, driving greater adoption of Nvidia hardware.

How do you overcome this flywheel if you are AMD, Intel, or even Apple Inc (NASDAQ: AAPL) itself?

I believe Nvidia's software/services could dramatically increase margins over time, thanks to this moat.

Tremendous growth already built into Nvidia shares

It all sounds impressive, doesn't it? It's probably why the company trades at more than 200 times earnings. The more bearish side of the argument is that nearly all of the upside is now priced in.

The more conservative fibre of my being tends to agree to an extent.

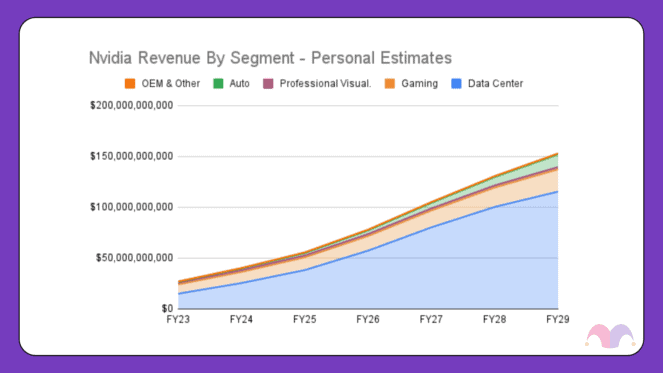

In my own long-term forecasts, I have estimated Nvidia's data centre revenue increases by nearly eightfold to US$115 billion in FY29. Additionally, potentially significant growth in gaming and auto places my total FY29 revenue estimate at US$139.6 billion, as shown below.

Assuming the company can derive more of its earnings from higher margin sources, such as software, the earnings growth could be just as colossal.

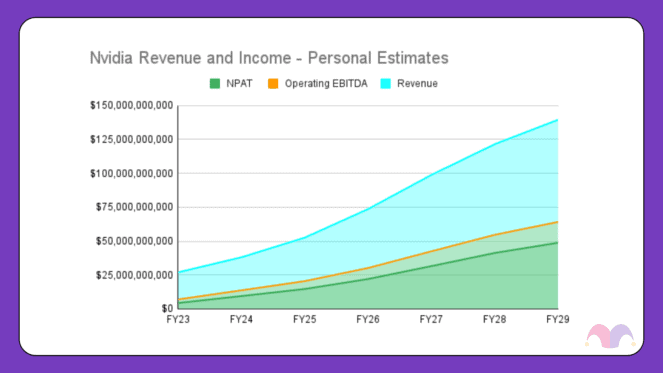

As Nvidia's more profitable data centre segment grows, I believe net margins could reach 35% by FY29. This would equate to a net profit after tax (NPAT) of US$48.9 billion — increasing more than 11 times from the company's FY23 profits, depicted in the chart below.

If Nvidia shares then traded on a 35 P/E, we could be looking at a US$1.6 trillion company. In other words, an annualised return of 10.5% per annum over the next six years.

Considering the average return of the S&P 500 over the past 150 years is 9%, that's a lot of execution risk for a slightly above-market average return.

What if AI demand peters out to a reduced level? What happens if a prolonged recession hits and cloud service providers need to cut back their capital expenditure? How would it all shake out if competitors posed a credible threat?

There isn't much margin of safety.

My verdict on Nvidia shares

In summary, I think Nvidia could become the operating system of AI. The company could very well be building a moat, the likes of which have never been seen before. In a decade or two, Nvidia has the potential to be worth trillions — yes, multiple — in my view.

At the same time, the current price makes it hard to see it as an asymmetric opportunity to the upside. It feels more evenly balanced at this point in time.

For now, I would be a holder of Nvidia shares. I certainly wouldn't be a seller, but I'd like to see a lower price before buying.