The ASX bank sector is a very competitive space. In this article, I'm focusing on two regional banks included in the S&P/ASX 200 Index (ASX: XJO), the Bank of Queensland Ltd (ASX: BOQ) and Bendigo and Adelaide Bank Ltd (ASX: BEN).

But which of these banks would investors be better buying shares in?

Both banks are considerably smaller than the likes of the big four, including Commonwealth Bank of Australia (ASX: CBA) and National Australia Bank Ltd (ASX: NAB).

However, they can be just as capable of producing good dividends and share price growth. So which of these challenger banks is better?

Let's look at one of bank investors' favourite reasons for owning stocks in the industry, dividends.

Projected dividend yield

Dividends might make up the bulk of the return from both banks over the next three to five years, unless their share prices perform very well.

According to the current estimates on Commsec, Bank of Queensland shares are projected to pay an annual dividend per share of 41 cents per share in FY23 and 42 cents in FY24. This would translate into grossed-up dividend yields of 10.7% and 11% respectively.

Turning to Bendigo Bank shares, they could pay an annual dividend per share of 60 cents in FY23 and 61.2 cents in FY24, equating to grossed-up dividend yields of 10% and 10.2% respectively.

On this measure, BOQ might pay bigger dividend yields, though that's partly because the BOQ share price has dropped so much in the last few months, as we can see on the chart below. It's down 22% since 28 February 2023.

BOQ's recent difficulties

It's important to acknowledge some major challenges that Bank of Queensland shares are facing.

This week we learned BOQ has entered into enforceable undertakings with APRA and AUSTRAC. This follows internal and external reviews leading to the identification of "deficiencies in its operational resilience, risk culture and governance and anti-money laundering and counter-terrorism financing program".

BOQ is going to address the identified weaknesses with an action plan that's due for approval within 120 days. It will also have an additional $150 million added to its operational risk capital requirement.

APRA said in its court-enforceable undertaking that "BOQ identified gaps in its risk culture in 2016, 2018, 2020, and 2022. However, BOQ's risk culture remained immature and BOQ did not prioritise risk culture uplift sufficiently over that time".

APRA also said that reporting to the BOQ board was "overly positive" and that BOQ didn't sufficiently "engage with regulators when heightened risks or significant issues arose". The regulator added:

APRA is concerned about, and BOQ acknowledges, the nature and extent of the Underlying Weaknesses, the Prudential Standard Breaches that these caused, the slow pace at which they were identified and the potential for new and significant prudential issues, including more Prudential Standard Breaches, to arise if the Underlying Weaknesses are not rectified as a priority.

BOQ said it has "already made good progress in strengthening its financial resilience and holds strong capital and liquidity buffers".

A key question in all this is whether it's a widespread sign of ongoing weakness in BOQ's quality, or whether it's a one-off problem that can be used to improve the bank's culture and structure going forwards. Either way, it's not a good look for Bank of Queensland shares.

Which ASX bank share is better value?

Both banks are facing a very competitive mortgage market. BOQ Chair Warwick Negus said in a shareholder letter that some mortgages in the market were being written "below the cost of capital".

The broker UBS recently noted the latest data from APRA showed in April, BOQ saw mortgage lending fall. In fact, it was the only bank on UBS's coverage list that saw mortgage lending decline, according to reporting by The Australian.

Thus, there are several factors going against BOQ at the moment. It's probably a good thing that Bendigo Bank is out of the limelight.

According to Commsec estimates, Bendigo Bank shares are valued at under 10x FY24's estimated earnings, while Bank of Queensland shares are valued at just over 9x FY24's estimated earnings.

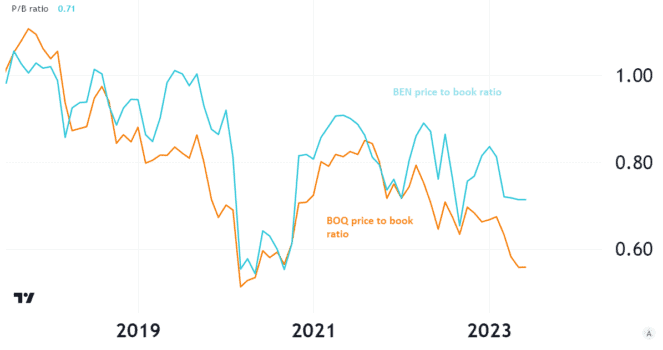

There's one measure where it may show that BOQ shares are attractively cheaper – the price-to-book ratio.

It shows the BOQ market capitalisation is trading at a cheaper price to its balance sheet than Bendigo Bank. However, there's more to being good value than just this ratio.

Out of the two, I'd choose Bendigo Bank. There's less going wrong for that bank at the moment and fewer distractions for management during this very turbulent period of higher interest rates.