Australians are fortunate to have many phenomenal listed companies at their fingertips. We have access to some of the most profitable banks in the world, globally regarded mining giants, and desirable brands on the ASX share market.

The Aussie market is 2,343 companies strong. Still, the local bourse represents only a fraction of the worldwide investable pool at a minuscule 2% of global market capitalisation.

To focus a portfolio solely on ASX-listed companies would be to starve it of some of the greatest investment opportunities the world has to offer, in my opinion.

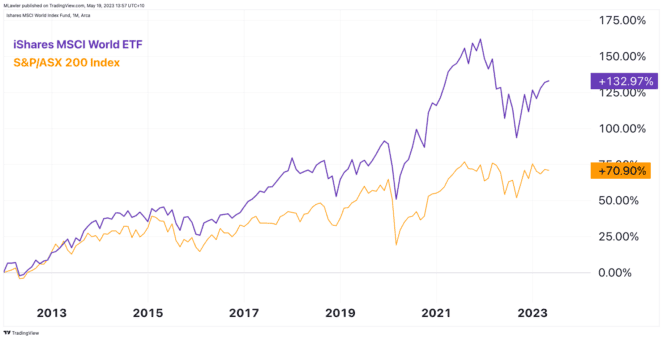

Not only that, but it also presents a risk in the form of geographical concentration. Putting all your eggs in one geographic basket could greatly underperform a more scattered approach. A quick glance at the S&P/ASX 200 Index (ASX: XJO) versus an MSCI World ETF since 2012, shown below, proves this point.

So let's chart a course. Destination? A truly global portfolio across several share markets.

Here are my top picks from seven different exchanges right now.

Image source: Getty Images

Where I'd go for global diversification

There are many more share markets than seven. However, I suspect the seven I've selected would be sufficient to get a decent cross-section of global equities. As with anything, the law of diminishing returns often applies.

My focus would gravitate toward companies in Europe, the United States, and the Asia-Pacific region (China, India, and Australia).

European share markets

1. Rightmove

The first cab off the rank is possibly my favourite opportunity abroad among this lot. Rightmove Plc (LON: RMV) is the largest online real estate property portal in the United Kingdom, pulling in more than 91 million site views last month. Its next closest competitor, Zoopla, trailed distantly behind with 31 million.

Think of Rightmove as the REA Group Ltd (ASX: REA) of the UK. However, Rightmove enjoys far greater margins and trades on a lower price-to-earnings (P/E) ratio (24 times) than REA Group (51 times).

In addition, the UK platform provider is debt-free with around A$75 million equivalent in cash. Whereas REA Group had a net debt position of $174.4 million at the end of December 2022.

With a track record of buying back stock, management has demonstrated its resolve to reward shareholders.

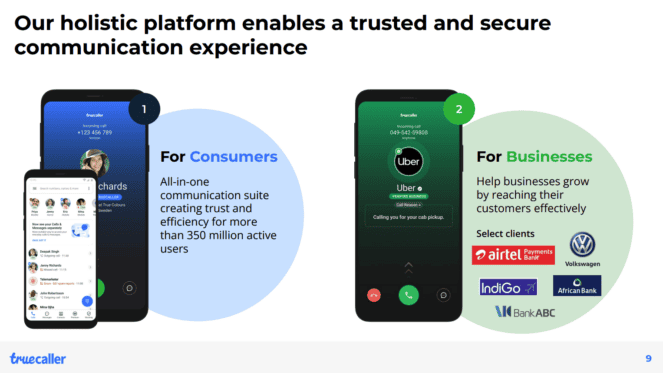

2. Truecaller

We have all contended with unwanted calls and texts. Not only are they a nuisance, but they can also be financially damaging. According to the Australian Communications Consumer Action Network, Aussies lost out on $1.4 million to scam texts in January this year alone.

Based out of Stockholm, Sweden, Truecaller AB (STO: TRUE-B) is a software company making communications "smarter, safer, and more efficient". Now trumpeting 344 million average monthly active users, it has become a leader in its space.

The bulk of Truecaller's revenue is derived from supporting advertising through its app. This accounted for roughly 80% of the company's latest quarterly revenue. Although, the business is making meaningful strides in growing its consumer and business subscriptions, pictured above, to diversify revenue streams.

Forecasts suggest Truecaller could grow its earnings at an annualised rate of more than 25% per annum moving forward. Yet, investors can buy a slice now at 26 times earnings. That seems like a fair price to pay for this solid business, in my opinion.

American share markets

3. Edwards Lifesciences

Listed on the New York Stock Exchange, Edwards Lifesciences Corp (NYSE: EW) develops a range of specialised healthcare products to treat structural heart diseases in a minimally invasive manner.

The medical technology company's main revenue source is its transcatheter aortic valve replacement (TAVR). Offering a solution for treating aortic stenosis (narrowing of the aortic valve) without resorting to open heart surgery has been pivotal in Edwards growing its revenue by 59.6% over the past five years to US$5,501 million for the 12 months ending 31 March 2023.

While the need for TAVRs is typically an age-related event, a generally unhealthy lifestyle can increase the risk of requiring intervention. Recently, a report has suggested more than half of the global population will be overweight by 2035.

In my opinion, Edwards is well-positioned to serve a growing aging and overweight population. At around 36 times earnings, it is also one of the lesser richly valued companies with exposure to this trend.

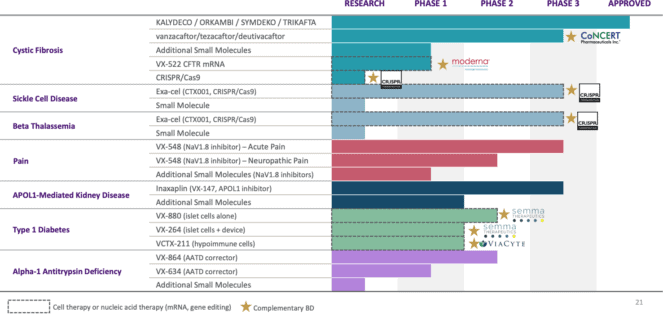

4. Vertex Pharmaceuticals

Sticking with US share markets, we have Vertex Pharmaceuticals Incorporated (NASDAQ: VRTX). However, rather than making medical devices, Vertex develops and commercialises therapies. Its most well-known product is Trikafta, a treatment for cystic fibrosis (CF) sufferers.

When it comes to improving the lives of people dealing with CF, Vertex is almost the only horse in the race at the moment. Impressively, the next closest competitor to Trikafta is another treatment being developed by Vertex.

Vertex enjoys net margins of more than 30%, holds in excess of US$10 billion in cash, and is parading several other drugs in development for other diseases (pictured above).

Despite this, the company is valued at 27 times its earnings. I wouldn't consider that expensive given the potential growth on offer here.

Asia Pacific share markets

5. Plover Bay Technologies

Few things are as important as internet connectivity in the modern world. These days, downtime in our network comes with a tangible, often high, cost.

Based out of Hong Kong, Plover Bay Technologies Ltd delivers "supercharged connectivity" to its customers across North America, Europe, the Middle East, Africa, and Asia. Through a combination of hardware and software, the company brings increased reliability to those who need it.

Networks are becoming increasingly complex. Businesses are tasked with utilising a combination of wired, wireless, or even satellite connection — depending on the application. Yet, Plover Bay is priced at around 14 times earnings.

I will say there is considerable customer concentration risk here. The company's top five customers accounted for 54% of total revenue at the end of 2022.

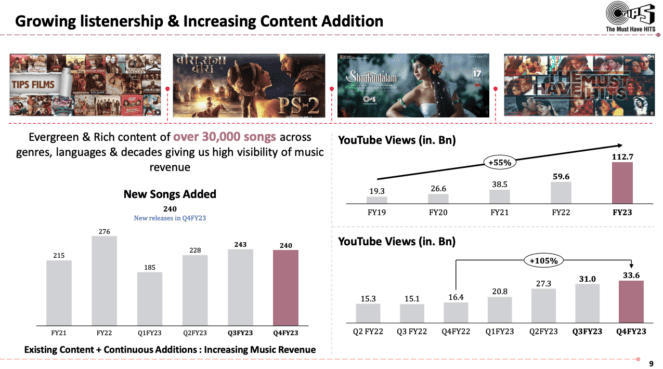

6. Tips Industries

Digital advertising continues to go from strength to strength, minting millions for those able to draw a substantial audience via their content. Just look at the incredible success of YouTube icon MrBeast.

Tips Industries Ltd is an Indian music record label and film producer. The company mainly makes money by collecting subscription and ad-supported revenue on music and films it holds the rights to. I like to think of it as the Universal Music of India.

What makes Tips appealing in my eyes is its profitability, its cashed-up balance sheet, and strong returns on capital. At an industry level, the Indian digital ad space is surging, increasing at an expected compound annual growth rate (CAGR) of 29% between 2018 to 2024.

As a result, Tips Industries would be my top pick within Indian share markets.

7. Macquarie Group

Finally, it is time for my top buy on our local share market, Macquarie Group Ltd (ASX: MQG).

The millionaire factory is arguably home to some of the most talented individuals in the finance and trading industry. Undoubtedly this has played a major role in the investment bank's astounding rise in profits over the last decade.

Although the outlook is gloomy for global economies, I find it hard to fathom how this company isn't meaningfully more valuable years from now. The management team is impeccable and Macquarie remains highly regarded in the industry.

At around 14 times earnings, Macquarie shares are looking far cheaper than they were two years ago.