There are countless ways of valuing businesses before deciding to pull the trigger on an investment. But, one often overlooked method for analysing an ASX share is its free cash flow (FCF) yield.

Essentially, the free cash flow yield measures the net cash generated by the company's operations relative to its enterprise value. The enterprise value is simply its market capitalisation, plus its total debt, minus its cash and cash equivalents.

Simply put, this metric is similar to the price-to-earnings (P/E) ratio, but for cash flows. You might be thinking: why not just stick with the good ole' fashioned P/E then?

Follow on to find out what the FCF yield offers over an earning multiple, what a good FCF yield is, and which ASX shares could be 'good' value based on this valuation method.

Why free cash flow yield can be useful

So much focus in the investing world is placed on earnings or net profit after tax (NPAT). However, the reality is this figure can sometimes be unintentionally misleading due to a variety of factors.

A common inclusion of a company's bottom-line earnings is non-operational income. Examples of this might include one-off asset sales or property valuation gains. In such cases, the listed entity suddenly looks dirt cheap based on its temporarily improved P/E ratio.

Unfortunately, unless one is privy to the earnings-altering items, there is a good chance someone could buy into the ASX share believing they've found a deal too good to be true.

Whereas, the free cash flow portrays a truer reflection of the returns generated by the company's operations.

Well, what is a good free cash flow yield? You might ask. Great question.

According to the legendary British investor and CEO of Fundsmith, Terry Smith, a 5% free cash flow yield is the minimum expectation.

During Fundsmith's 2013 shareholder meeting, Smith explained:

I will only buy companies that have a free cash flow yield which is about 5% or more. The reason for that is if I buy those companies with that yield that is higher than those [4% to 4.5% yielding] bonds I can be sure of one thing… over the long term the free cash flow yield of our companies will rise […] I can be equally sure the coupon (yield) on the bonds won't go up.

In other words, Smith seeks to own companies that generate a greater expected return than bonds. Which makes sense. If you didn't think you could get a better return from your ASX shares, you'd buy bonds instead.

Next question… which companies listed in Australia fall into this 'above 5%' FCF yield category?

I'm glad you asked.

Which ASX shares are yielding more than 5%?

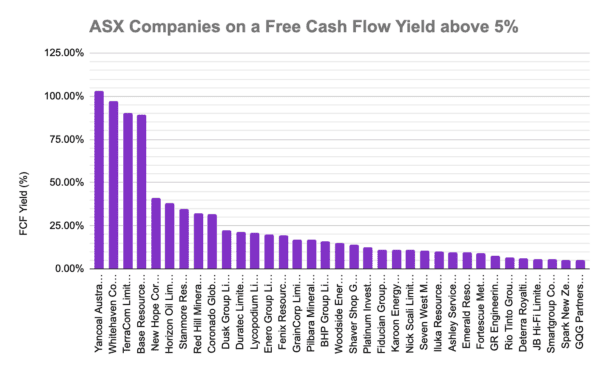

There are 35 companies on the ASX with a market capitalisation above $100 million and a free cash flow yield above 5% (as of Tuesday afternoon). Additionally, these companies posted a return on capital above 15% in the last 12 months, which is generally considered good.

The ASX shares with the highest FCF yield include coal shares Yancoal Australia Ltd (ASX: YAL), Whitehaven Coal Ltd (ASX: WHC), and Terracom Ltd (ASX: TER) as shown in the chart above. However, coal prices have fallen since the end of 2022, which could lead to a dramatic reduction in future cash flows.

Buying opportunities?

Most of the companies that make the cut are highly cyclical. This means they may not be the best fit for a portfolio if someone is looking for defensive ASX shares.

In saying that, there are still a few businesses that catch my eye as potential buys due to their sturdy balance sheets, growth history, dividends, and free cash flow yield.

Although retail shares could be prone to a weaker economy, the likes of Nick Scali Limited (ASX: NCK), JB Hi-Fi Limited (ASX: JBH), and Dusk Group Ltd (ASX: DSK) look relatively attractive. The share prices of these companies are down 5.6%, 8%, and 34% respectively over the last year.

Personally, I believe JB Hi-Fi is the pick of the bunch given its exceptionally cashed-up balance sheet. At the end of December 2022, the retailer held $391.2 million in cash and zero debt. And, its FCF yield is around 5.7%, surpassing Terry Smith's bar.