The Fortescue Metals Group Ltd (ASX: FMG) share price is ahead of the benchmark over the past year, but is it still worth buying?

Shares in the Australian iron ore miner are 4.3% better off than this time last year, as shown below. Meanwhile, the S&P/ASX 200 Index (ASX: XJO) is down roughly 3%. The return from the Andrew Forrest-led company is also healthier than similar ASX-listed peers.

After diverging from the market's trajectory, is Fortescue primed to run further — or could it be time to look elsewhere for outperformance?

We took this question to two of our team to gather some perspective on both sides of the tape. Read on to find out where this instalment's bull and bear agree and disagree on the path forward for Fortescue.

Carving out a spot in the portfolio for Fortescue shares

By Tristan Harrison: Fortescue shares have performed well over the last six months. Certainly, it would have been much better to buy half a year ago at a price under $18 compared to today's valuation. Fortescue shares closed on Thursday at $22.42 a share.

However, I believe the business can perform better than expected from here.

Firstly, no one knows what iron ore prices are going to do next month or next year. If we went back 12 months and looked at where brokers thought the Fortescue share price would be or what the dividend payout ratio could fall to we'd see that some of those predictions haven't eventuated.

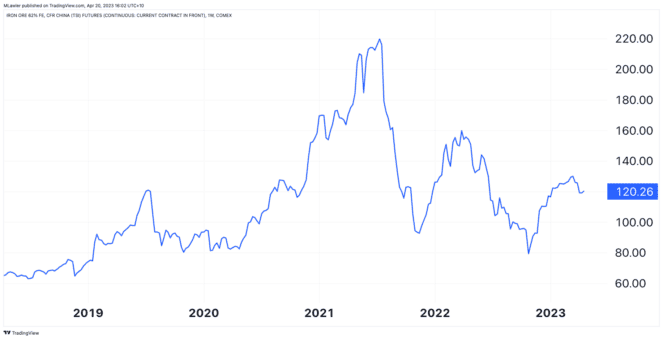

Undoubtedly, Fortescue has been helped by the stronger iron ore price, which is currently sitting at around US$120 per tonne, displayed below.

The iron ore price could continue to be stronger than expected, partly helped by improving Australia-China relations. A better-than-expected iron ore price could mean stronger profits, stronger dividends, and enable more funding for Fortescue Future Industries (FFI).

Fortescue is also close to production for the Iron Bridge project. This could add millions of tonnes to its total output, which would boost earnings. In the longer term, it's looking to diversify its production by expanding into African iron.

The ASX mining share is also looking to produce green hydrogen and green ammonia, which would be emission-free fuel for heavy machinery, boats, and perhaps planes.

It's progressing a number of potential green energy projects around the world, with multiple projects expected to advance this year. FFI has already signed multiple agreements with prospective energy customers, with Europen energy giant E-ON being the biggest so far.

The price tag of its green energy efforts may be less intimidating when we take into account comments by FFI boss Mark Hutchinson to the Australian Financial Review. Hutchinson said that FFI could/"will" sell equity stakes in its green hydrogen projects, which would reduce the amount of capital Fortescue needs to set aside. I think this could enable a better-than-expected dividend payout ratio.

Fortescue boss Andrew Forrest has previously revealed investment banks have suggested that FFI could already be worth US$20 billion if it were listed, and that potential value isn't recognised on Fortescue's balance sheet.

Motley Fool contributor Tristan Harrison owns shares in Fortescue Metals Group Ltd.

Why be a bear about it?

By Brooke Cooper: To begin, I agree with Tristan; Fortescue's hydrogen and green energy efforts could lead to a dazzling future for the company. However, I believe its planned transformation could come at a high cost for both it and new investors.

While hydrogen and green energy offer mountains of potential, becoming a leader in the space also demands mountains of cash.

Fortescue has in place a $9 billion plan to decarbonise its Pilbara operations by 2030. Most of that investment is slated to be spent between financial year 2024 and financial year 2028. Key to the scheme is Fortescue Future Industries (FFI).

The operation can be allocated up to 10% of the iron ore miner's net profit after tax (NPAT). It's expected to demand between US$500 million and US$600 million of operating expenditure and US$230 million of capital expenditure this financial year.

What might this spending mean for investors? Well, such transformational growth will take time. Meanwhile, the company's dividends could bear the brunt of its green ambitions.

Indeed, Goldman Sachs expects the ASX 200 iron ore miner to drop its dividend payout ratio and raise additional debt to fund its green ambitions.

Looking forward, the broker forecasts the company will hand out US$1.82 per share in dividends this fiscal year, US$1.10 next fiscal year, and 79 US cents in fiscal year 2025.

At that rate, Fortescue's dividend yield could more than halve over the next two financial years, considering its current share price and today's exchange rate.

But the company is, of course, an iron ore miner at heart. On that front, the broker recently found it's more expensive on a price-to-net-asset-value (NAV) ratio than its major peers.

Take a look:

| ASX 200 iron ore miner | Price to NAV |

| BHP Group Ltd (ASX: BHP) | 0.95 times |

| Rio Tinto Ltd (ASX: RIO) | 0.85 times |

| Fortescue Metals Group | 1.44 times |

All in all, I think Fortescue's green ambitions have the potential to provide strong returns in the future. However, I don't think the risk-to-reward ratio currently on offer is worthwhile.

Motley Fool contributor Brooke Cooper does not own shares in Fortescue Metals Group Ltd, BHP Group Ltd, or Rio Tinto Ltd.