I'm a big believer in regularly buying ASX shares, regardless of what is currently going on in the world — through the good and bad times. For me, that means adding to the portfolio at least every month. For April, it is PWR Holdings Ltd (ASX: PWH) that has caught my attention.

At the time of writing, the maker of cooling solutions for high-performance vehicles is currently trading at $10.09 per share. This corresponds with an 8.1% fall in the company's share price since the beginning of the year.

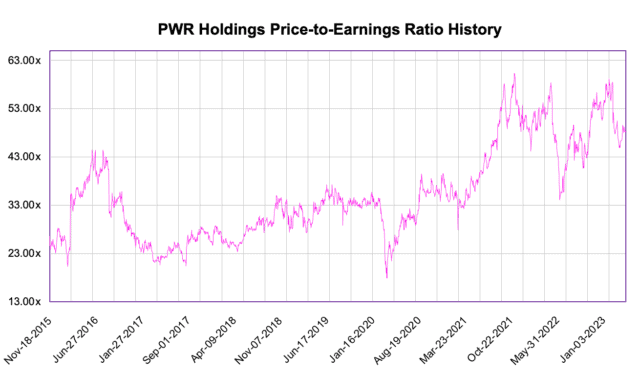

PWR Holdings is a high-quality ASX share with a price-to-earnings (P/E) ratio of 49 times. While this might deter some investors, I believe there are compelling reasons to consider adding it at its current valuation.

In this article, I'll be sharing five compelling reasons why I personally find PWR shares an attractive investment opportunity in April.

5 reasons to buy PWR shares this month

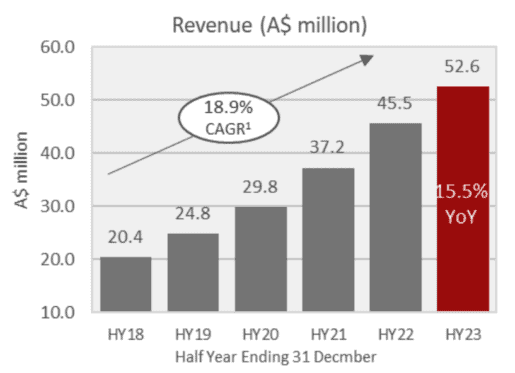

1. PWR Holdings' revenue has grown at an 18.9% compound rate

At face value, the high-performance parts manufacturer might look extremely expensive. While it trades at a P/E multiple of nearly 50 times, the global auto components industry average hovers around 20.

However, unlike most of its peers, PWR Holdings is growing at a phenomenal rate. As pictured below, the company's revenue has grown at a compound annual growth rate (CAGR) of 18.9% over the past five years.

Since 2014, the top line has increased each and every financial year. That level of consistent growth deserves an above-average earnings multiple, in my opinion. If PWR can maintain a 15% per annum growth rate moving forward, its full-year revenue could double to $217 million in five years.

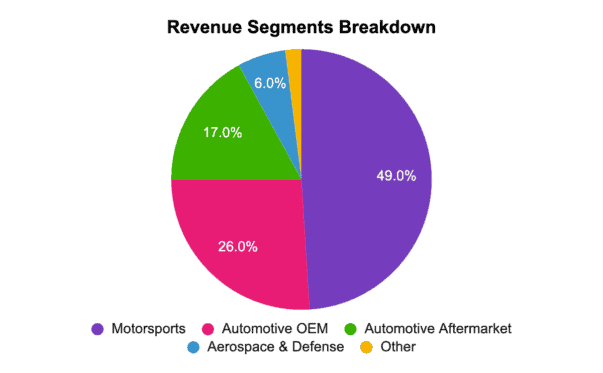

2. Diversified revenue streams — ready to weather a weak economy

A weaker economy is possibly on the cards as interest rates chew up their fair share of consumer spending. Although the short-term pinch will become less significant with time, it sure helps to ride the wild wave by being diversified.

Fortunately, PWR Holdings doesn't rely upon one source for its revenue. As the diagram below shows, income is spread across several segments including motorsports, automotive OEM, automotive aftermarket, and aerospace and defense.

In my opinion, the aerospace and defense segment could achieve considerable growth even under tough economic conditions. The potential financial padding this avenue offers is another reason why PWR shares are appealing to me at the moment.

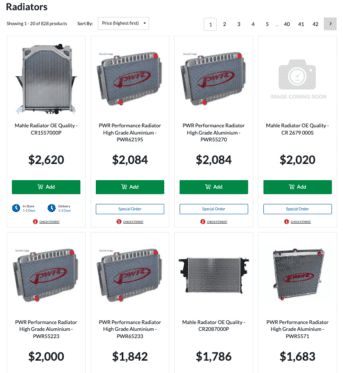

3. Competes on quality and performance, not price — hello pricing power!

Inflation is expected to remain above 3% out to mid-2025. If companies don't have some form of pricing power, this will crimp earnings margins.

One form of pricing power that I believe PWR Holdings has is superior quality and performance. That means the company's products don't necessarily need to compete on price, making it easier to pass on higher costs.

This is evident when browsing an automotive store, such as Repco, for radiators (pictured above). PWR's products are prominently featured in the highest-priced radiators and are noticeably absent from the cheapest options.

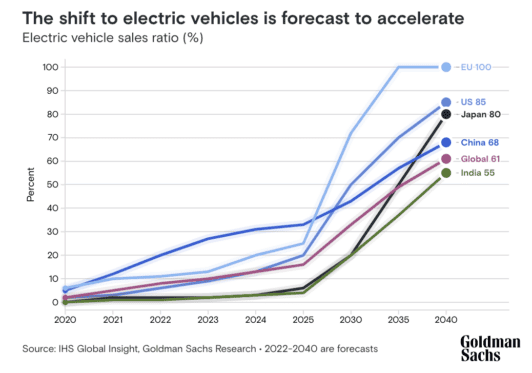

4. Tapping into a growth industry

P/E ratios can be a poor means of valuing a company if future earnings accelerate rapidly. This could be the case for PWR shares, in my opinion, as the company latches onto a fast-growing market.

Forecasts shared by Goldman Sachs suggest electric vehicles (EVs) could make up a substantial share of total vehicle sales by 2040. For example, Europe EV sales are expected to grow from 11% in 2022 to 100% by 2040, as shown in the chart below.

Every EV needs some form of battery cooling technology — something that PWR Holdings management has said they're 'well placed' to deliver on.

The increased adoption of EVs is a market for PWR's expertise that I think is being undervalued.

5. PWR share price might not be factoring in greater growth for longer

This point echoes the underlying reasoning of the last, but the market might be underestimating PWR's future earnings ability.

As I previously mentioned, if PWR were to double its revenue in five years — while maintaining its profit margins — the P/E ratio would halve to 25. But what if the company's earnings were to double again over the next five years? Suddenly the earnings multiple is closer to 12.

Given the growing market potential across multiple decades, I believe the current 50 times multiple could end up looking like an opportunity in hindsight.

This is the main reason why I'm seriously considering buying PWR shares this month.

Is it enough to buy PWR shares over other ASX shares?

The hardest part of being an investor is deciding which mouths to feed. There are usually several options vying for investment, but limited capital makes it important to fuel the best at the time.

This month, the top companies on my list for deploying my spare funds include Apple Inc (NASDAQ: AAPL) and Macquarie Group Ltd (ASX: MQG) — both of which are existing holdings. However, the exceptional growth potential offered by PWR shares positions it as my top April buy on the ASX.