Finding an investment that ends up delivering a return of more than 100% in six months is remarkably rare. Yet, that's exactly what has occurred with the Weebit Nano Ltd (ASX: WBT) stock price.

What is even more extraordinary is it would have been 246% if I was writing this 39 days ago. The resistive random-access memory (ReRAM) developer attracted strong buying throughout January and February, as shown below.

During this time, Weebit entered the S&P/ASX 300 Index (ASX: XKO) and drew closer to its commercialisation efforts. Notably, the company taped out its first 22-nanometre demo chip for manufacturing in January, inching closer to a viable product.

I knew of Weebit Nano six months ago, albeit not one I closely watched, but chose not to buy (or even add to my watchlist). Turns out the choice meant missing out on a 130% return in a small space of time.

Why I didn't buy Weebit Nano stock

There will always be plenty of missed opportunities as an investor. I tend not to dwell on missing out, but it doesn't mean there aren't insights that we can gain by undertaking a little introspection.

Furthermore, the most important assessment to make is whether your decisions are congruent with your investment strategy. If passing on a stock that ends up returning 500% means sticking within the bounds of your overall risk tolerance, that's a win in my books.

When I ask myself the question: Why didn't I buy Weebit Nano stock six months ago? there are a couple of reasons that immediately spring to mind.

The most obvious reason why I didn't give Weebit the time of day is its early product development stage. I commend the team for how far they have come so far. However, the company is still yet to prove the economic viability of its chips.

And, yes, I understand that it's commonplace that these types of businesses typically work towards a buyout rather than operating commercially on their own.

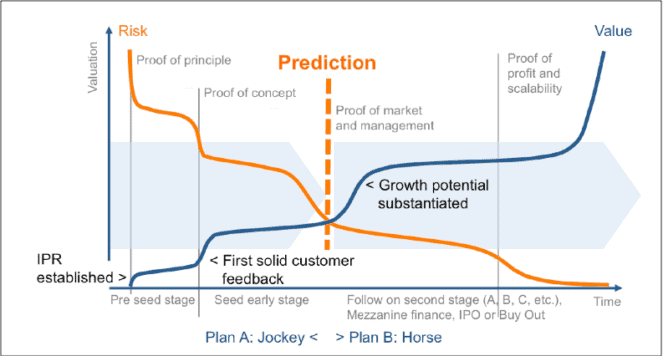

Though, it doesn't change the fact that I believe Weebit is still between the proof of concept and proof of market stage — situated too high along the risk curve, depicted below, for my liking.

Secondly, I'll be the first to admit my knowledge of resistive RAM is sparse. In my opinion, the smaller you go in company market capitalisation, the deeper the knowledge needed in the relevant industry to have an edge.

Unfortunately, I'm not up with the latest in advanced memory technologies. It sits outside my area of competence. Yet another reason why the Weebit Nano stock didn't make it onto my radar six months ago — let alone buy it.

What I would need to see

While I'm doubtful that Weebit Nano would ever make it into my portfolio due to my lack of expertise on the subject matter, there are conditions for potentially making an exception.

Firstly, the chip developer would need to fully commercialise its memory technology. That means drawing meaningful operational revenue from the licensing of its intellectual property or direct sales of its memory chips.

From there, I could at least analyse the unit economics of the technology to project whether it could scale to profitability. Until then, any investment in Weebit Nano stock is highly speculative in my opinion.

That's fine if speculation is the aim. However, it's not what I'm looking for in a long-term investing strategy.