Earnings for this healthcare giant were slashed by a colossal 54% in the first half, yet I'm hungrier than ever for more Sonic Healthcare Ltd (ASX: SHL) shares.

On Thursday, shares in the laboratory, pathology, and radiology services provider blasted 14.2% higher despite revenue and profits cratering. On top of that, the figures presented missed consensus estimates by 1%.

So, why on earth would I be wanting to increase my stake in Sonic Healthcare now?

At present, the company holds a 1% weight in my portfolio. Ideally, I'd now like to grow that position to between 2% to 3%… and here's my reasoning.

The COVID comedown

It's no secret that COVID-19 testing provided a temporary tailwind to Sonic's top and bottom lines. We are now seeing that fade away as we return to our 'new normal'. The diminishing COVID revenues have been an anchor on the Sonic Healthcare share price over the past year.

This might be unnerving for some shareholders. However, I take solace in the fact the core business is now fundamentally stronger than it was prior to the PCR testing frenzy.

As noted in its first-half results, Sonic's 'base business revenue' — comprising of laboratory, pathology, radiology, etc. revenue excluding COVID-19 testing — increased by 9% compared to the prior corresponding period to $3.7 billion.

Prior to 2020, the company had been growing its top line at around 10% per annum on average. I think there is an underappreciation for this base revenue. While it's not a trendy new industry, the diagnostic services market is incredibly large and estimated to grow at a compound annual growth rate (CAGR) of 13% out to 2030.

Where will Sonic Healthcare find growth?

I believe Sonic Healthcare will be able to sustain its 10% revenue growth by expanding into higher value — and possibly more in-demand — areas of diagnostics such as genetic, microbiome, and molecular diagnostics.

Molecular diagnostics

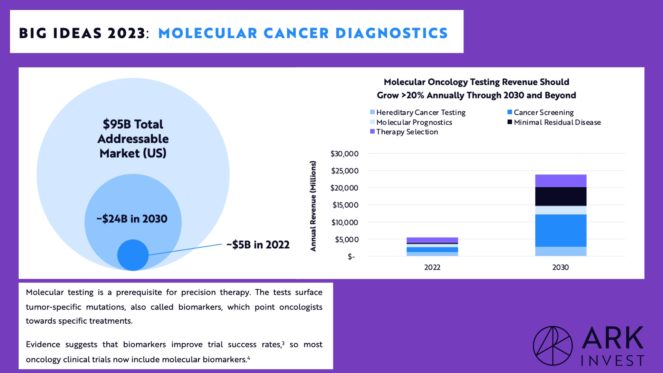

Speaking of molecular diagnostics: this is an area of diagnostics that Ark Invest highlighted in its Big Ideas 2023 report.

Analysts at Ark estimate the total addressable market for this type of diagnostic testing for cancer alone could be US$95 billion. Likewise, annual revenue derived from this form of testing is forecast to grow above 20% per annum through 2030 and beyond.

My guess is this played a key role in Sonic's decision to acquire ProPath in 2021. ProPath is a specialist in molecular pathology, serving 1,000 physicians and more than 20 hospital groups in the United States.

Hence, the addition of ProPath taps into the potential growth engine of molecular diagnostics — enabling a path for more upside in Sonic Healthcare shares.

Aging population

In my opinion, Sonic Healthcare could also grow faster for longer than most investors think due to an aging population. As people live longer as a byproduct of medical advancements, the rate of occurrence of cancers could trend higher.

As pictured above, the burden of cancer is estimated to increase by more than 60% from 2018 to 29.4 million new cases globally in 2040. In turn, I believe the demand for genetic predisposition testing, diagnosis, and prognosis of cancers will similarly expand over the next two decades.

There was an early indicator of the high growth rate in this market within Sonic's half-year presentation. In the US, revenue growth from ThyroSeq (thyroid cancer genetic test) was above 25%.

The potential reacceleration of earnings growth from this structural tailwind plays a significant role in my desire to buy more Sonic Healthcare shares.

What else is appealing about Sonic Healthcare shares?

There are a few others reasons why I personally see more upside to this global healthcare giant. To avoid this article becoming more of a novel, I'll list these additional positive factors below:

- Despite COVID-19 testing revenue diminishing, molecular testing for various viruses will undoubtedly persist in the future.

- The company is positioned for further inorganic growth as management utilised COVID-19 profits to deleverage its balance sheet.

- Plenty of runway for increased dividends or more buybacks

Lastly, my ultra bull case for Sonic Healthcare shares is centred around where value will accumulate along the value chain in the future.

I believe there is potential for laboratory testing to absorb a greater proportion of attributed value as the industry pivots to a preventive approach, rather than reactive. Greater margins could be recognised by the likes of Sonic as a result.

This is quite a speculative assumption. Realistically, such a scenario is purely the 'cream on top' of my investment thesis.