It is hard to believe that the Vocus Group Ltd (ASX: VOC) share price was trading at over $9 only a few years ago and around $4.50 more recently when it was a take-over target.

Yesterday the Vocus share price slid back down below $3, closing at $2.94. Is it time to consider a buy?

The turnaround strategy

Vocus has been simplifying its business to three independent operations – Network services, Retail and New Zealand. After a spree of acquisitions, simplifying its structure makes sense and should help with reducing costs and frictional inefficiencies. It also plans to turn around its Retail segment and has developed a 5-year pipeline of strategic fibre builds.

The core business

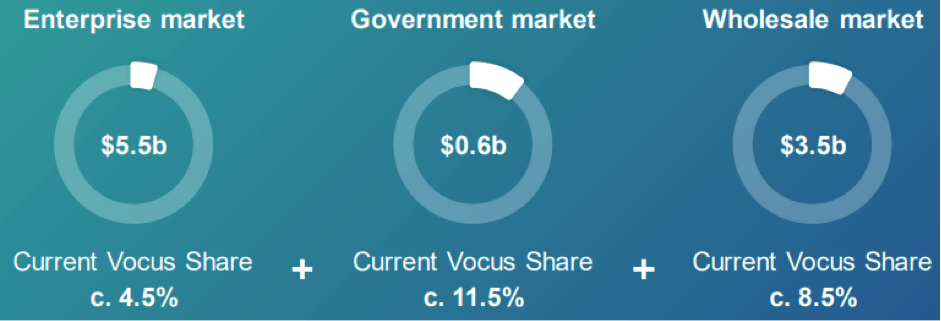

Vocus' core business is the network services segment. Here, Vocus is the leading fibre and network solutions provider where it targets enterprise, government and wholesale markets and recently completed its Australia–Singapore cable project. This has given it a first mover, highly competitive advantage with a strong demand for data and traffic moving to the west.

The growth potential

Vocus believes the network services market has untapped growth potential with its current market share showing there is still significant ground to gain as shown in the below chart.

Source: Vocus company announcement

The increase in data growth

Vocus New Zealand has seen a significant growth in data usage with the percentage of consumers with non-capped data rising to 71% in 2018 from a mere 8% in 2014. The company has seen a 92% broadband uptake where it notes broadband as being the entry point into the home for it to then sell more products such as mobile, electricity or gas.

Vocus Retail plans to draw from this experience where consumers prefer a single billing experience and is easier to upsell other products.

New management coming

In October, Vocus announced its new CFO who will be commencing in January 2020, succeeding outgoing CFO Mark Wratten.

The new CFO, Nitesh Naidoo has led finance teams in global companies for over 20 years and is a highly experienced telco executive who joins from Optus where he was vice president.

Guidance

Vocus met its FY19 guidance and has projected a mostly flat guidance for 2020 where it expects a stronger second half. It has also forecasted earnings before interest, tax, depreciation and amortisation growth in Vocus Network Services of $20 million–$30 million, which will be offset by a similar decline in its retail segment.

Vocus expects to see sustainable profitable growth in 2020 and beyond for its core business of Network Services. It expects diversification of revenue and cost saving opportunities to return to the Retail segment and believes its strong New Zealand business is positioned for further growth.

Foolish takeaway

It was good to see Vocus hit its guidance for FY19 and it does appear to be getting back on track for future growth after some difficult times. I currently own Vocus shares and, however tempting the current share price is, I would consider waiting for the 2020 financial results before making a decision to buy more or make an initial investment.