Shares in agricultural REIT Rural Funds Group (ASX: RFF) are down 19 per cent over the last six months as it struggles to shake off allegations of a conflicted management structure by short sellers.

On November 21 Hong Kong-based short selling research house Bucephalus took aim again at the management structure where Rural Funds Management (RFM) acts as responsible entity (RE) on behalf of the listed RFF investors.

Bucephalus also took aim at RFF's plan to sell its poultry assets. Bucephalus claims RFF underinvested in them for many years to the point where they're now no longer profitable.

Bucephalus claims the decision to sell is because it wants to strips out the cash to maintain dividends, etc, while the actual value of the RFF unit holders' assets is being slowly run down.

Rural Funds has dismissed these allegations as nonsense.

Rural Funds Management has also repeatedly dismissed the allegations that it's using cash and equity raisings to prop up the dividends paid by RFF to its unitholders.

It has also rubbished allegations that it's running RFF to enrich RFM management due to a remuneration structure that includes RFM's fees being based on RFF's net asset values.

It even went as far as paying auditor Deloitte to look into a number of allegations from original short seller Bonitas Research and dismiss them all as unfounded.

The decision to not comment on Bonitas's allegations and instead point investors to the 'audit assurance' and commission a separate Deloitte report was unusual.

Investors are free to draw their own conclusions as to why Rural Fund's management went for this "Fifth Amendment" no comment type approach.

If an RE in any trust-equivalent type structure earns fees on the percentage of asset value (rather than income generated for example) it will earn more fees if asset values go higher over the short term.

Asset values could rise through a mix of equity raisings and debt at RFF, among other things.

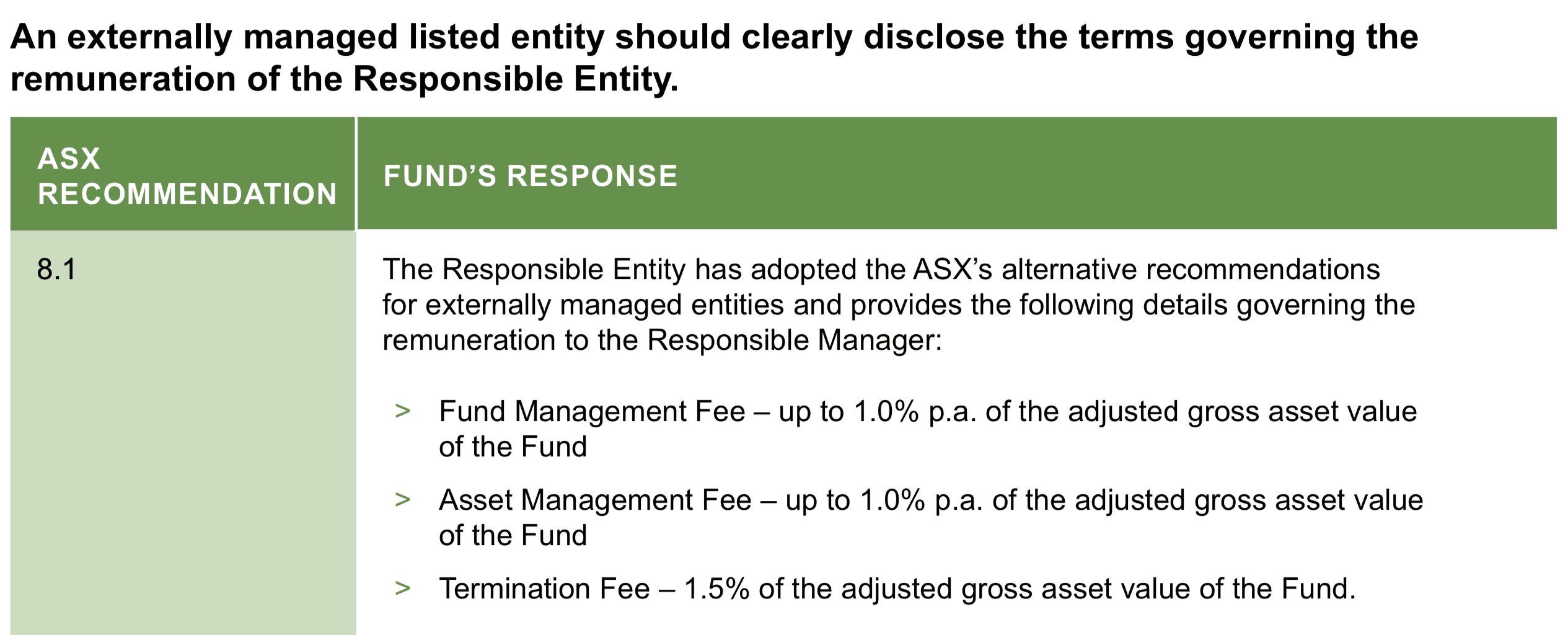

Below I managed to find the disclosure of the fee structure in Rural Funds Management latest annual report.

Source: Rural Funds annual report to 30, June 2019.

Asset values are based on yields so if they are high over the short term so should be the asset values, but if they're underinvested in over the medium term the scheme may start to suffer.

More importantly, this kind of RE to investment manager fee scheme is bog standard in the equity or securitised debt asset management industries for example.

The difference is that an RE in the say the equity asset management industry has no control over asset values. It's simply dependent on stock market movements and the investment manager's trading decisions as to the level of FUM.

Of course the higher the FUM for the RE the better, but it has no control over inflows or outflows. It only provides administrative services by appointment and any other fund accounting services or the like by appointment.

Rural Funds' management structure is different and it's working in the agricultural asset management industry that is far more subjective (in terms of valuation), opaque, and hard to get your head around.

RFF also has a tonne of debt.

For its part Rural Funds' management insists there's nothing to worry about as the groups' interests are mutually beneficial.

It also insists the sale of the poultry assets for $72 million is a good deal and part of the long-term plan to reinvest into better assets.

It also reports it's on course to pay dividends of 10.85 cents per share on earnings of 13.4 cents per share over FY 2020.

I am not a buyer of shares myself though.