Picking companies you'd like to hold for the next two decades is always easier in hindsight. You can look back now and wish you'd bought CSL Ltd (ASX: CSL) shares for $2.50 back in 1994. But unfortunately, we don't have this luxury for the future. We can only make decisions based on what we know from the present and past, so I've picked three ASX shares that I think show potential for a long-term hold.

So here's my case for owning Ramsay Health Care Ltd (ASX: RHC), Coles Group Ltd (ASX: COL) and Washington H. Soul Pattinson and Co. Ltd (ASX: SOL) for the next twenty years.

Ramsay Health Care

Founded in 1964, Ramsay Health Care is Australia's largest private hospital operator, owning or operating over 220 hospitals across Australia as well as the United Kingdom, France, Indonesia and Malaysia. If you had bought Ramsay Health Care shares for around $1 back twenty years ago, you would be sitting on a price gain of 6,364% – you guessed it, at the time of writing one RHC share will set you back $64.64. And that's not even including the dividends.

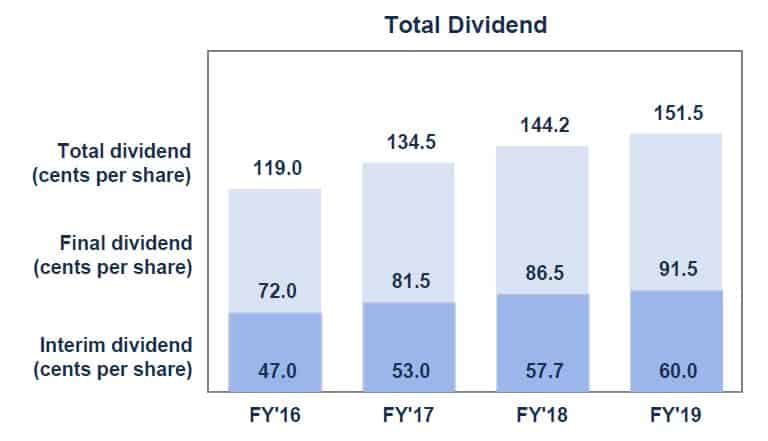

Although Ramsay offers a seemingly unimpressive starting yield of 2.34% today, it has increased its dividend every year since 2000 (some of which you can see in the table below) – one of only two ASX companies to offer such a track record (more on that later).

Source: Ramsay Health Care

Such an impressive history of growth and income over the past twenty years is enough to warrant a further look into whether Ramsay might be a strong buy for the coming two decades.

And I think it is.

For one, Ramsay's management is extremely talented in turning cash into more cash. The company's trailing return on equity (which measures this ability) has averaged 20.93% over the last twelve months – a very pleasing sign.

But I think the real reason to look into this company is the tailwinds its business sits in. We all know our population is ageing, and so demands on the healthcare system are only going to grow over the coming years. But I think the real opportunity for Ramsay is its private nature. Healthcare costs and Medicare take up a significant (and rising) chunk of both state and federal government spending. Due to our ageing demographics, this will become harder and harder to fund without raising taxes, which we all know is very unpopular.

There are already substantial government incentives for the wealthier members of the population to take private health cover and use private hospitals like the ones Ramsay runs. I believe these will only increase as Medicare costs rise – giving more and more people a dangling carrot in front of a Ramsay hospital door.

So yes, for the above reasons I think Ramsay qualifies as a company worth holding for the next two decades.

Coles

Coles is quite a new player on the ASX block – only coming into its own in November last year when it was kicked out of its parent company Wesfarmers Ltd (ASX: WES)'s nest. Wesfarmers still owns a 15% stake in Coles, so clearly they see some value in holding a stake of Australia's second-largest grocery chain going forward. But I think Coles is also a company worth holding on to for the coming decades.

Post spin-off, the Coles Group consists of the Coles supermarkets, as well as the Coles Express service station convenience stores and the Coles Liquor network (which consists of the Liquorland, Vintage Cellars and First Choice bottle shops). The company also owns a small network of pubs/hotels through a subsidiary arrangement.

Food, household essentials and alcohol are all highly resilient areas of consumer spending. If a recession comes (almost inevitable over the next two decades), people aren't going to stop buying food, washing powder, razors, wine or cigarettes from Coles. In fact, shoppers who might have gone to more boutique upmarket grocers might be drawn back to a cheaper grocer like Coles in tough times. This gives Coles an edge over many other investments in my view, and should also ensure a fairly safe dividend.

Speaking of dividends, Coles has announced that its first dividend will be a payout of 35.5 cents a share. This should mean that the company's FY20 yield will be around 3.5% based on current prices (or 5% grossed-up).

Looking forward, I think Coles' investment in automating its supply chains and reducing staffing costs as well as its investments in the online shopping space will translate into a thriving company in two decades' time (with a hefty dividend to boot).

Washington H. Soul Pattinson and Co

Washington H. Soul Pattinson or 'Soul Patts' as it's commonly known, is the closest thing on the ASX to Warren Buffett's legendary investing conglomerate Berkshire Hathaway. Although it owns and operates a small chain of pharmacies (its original raison d'être), today the company makes most of its money from investing in other ASX businesses which its management think will return long-term value to its shareholders.

Some of its current holdings include

- a 25.3% ownership in TPG Telecom Ltd (ASX: TPM)

- a 50% holding of New Hope Corporation Limited (ASX: NHC)

- a 44% stake in Brickworks Ltd (ASX: BKW)

Soul Patts is careful about selecting a portfolio of businesses that will deliver cashflows in good times and in bad – which they have proven very good at if history is anything to go by. Since its ASX listing in 1903, the company has never failed to pay a dividend and has (along with Ramsay) been increasing said dividend every year since 2000.

Since this company was able to keep its dividends up during the GFC, I think that alone proves its worth. Its current payout ratio is just 57%, which gives me reason to believe Soul Patts has plenty of dry powder and will likely keep bumping up its shareholder paycheques over the coming two decades. Soul Patt's diverse earnings base and superfluous dividend history make this a stock I want in my portfolio not just for the next decade or two, but for the rest of my life.

Foolish Takeaway

I think these three ASX companies give us enough past and present information to make a fairly good call that they would be worth holding for the next two decades. Of course, finding a good price is always half the battle, but I'll leave that up to you, Fool!