The BWX Ltd (ASX: BWX) share price will be on watch on Thursday after the personal care products company released a trading update based on its performance through to November 30.

According to the release, weak trading means that management has downgraded its FY 2019 normalised earnings before interest, tax, depreciation and amortisation (EBITDA) guidance to be in the range of $27 million to $32 million. This compares to its previous guidance of normalised EBITDA broadly in line with FY 2018's $40.3 million.

In addition to this, management had previously stated that 70% of its earnings were expected to be generated in the second half. It now expects first half normalised EBITDA of $7 million, meaning there will be a skew of 74% to 78% to the second half.

Why is the company underperforming?

Management has blamed the underperformance on a number of factors. These include softness in domestic export trading sales to China, the temporary loss of sales momentum in core U.S. brands, and some recurring Sukin Domestic ERP start-up issues in early October.

BWX CEO and managing director, Myles Anceschi, said: "It is disappointing that China volumes were weaker than expected. We have further refined our go-to-market strategy to improve pricing controls, and ownership by signing an exclusive distribution agreement effective December 2018, that will yield more focused efforts on growing this high-growth export channel with an established partner."

In respect to the slowdown in U.S. sales, Mr Ancecshi said: "In the US, we experienced a loss of sales momentum in our core US brands (Andalou Naturals and Mineral Fusion) during the management transition. Our new US senior leadership team has been appointed with a Senior VP of Sales starting with the company in December, and a Senior VP of Marketing commencing in January 2019. Some softening has also been seen in the most recent 12 week US retail sales numbers, which we are monitoring closely."

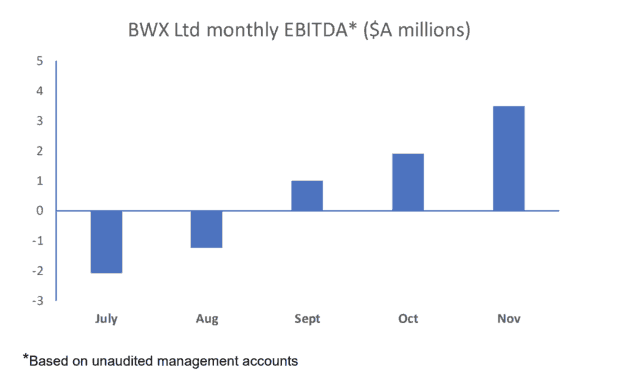

One positive is that BWX's performance is certainly improving as the year progresses, as you can see below.

Should you invest?

Although its shares look cheap after its sizeable decline this year, I'm holding off an investment until I've seen a big improvement in its performance.

Until then, I think fellow exporters A2 Milk Company Ltd (ASX: A2M) and Bellamy's Australia Ltd (ASX: BAL) would be better options for investors.