The worst performer on the All Ordinaries today has been the Netcomm Wireless Ltd (ASX: NTC) share price by some distance.

At the time of writing the broadband equipment company's shares are down a massive 40% to 82 cents following the release of its full year results.

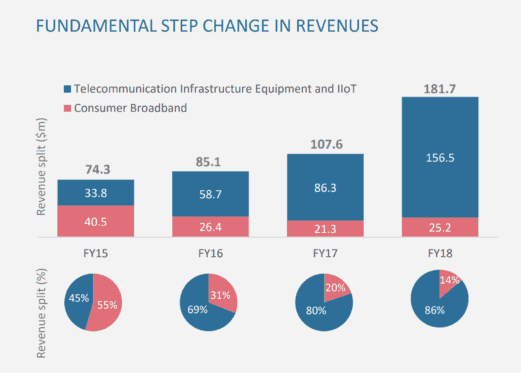

For the 12 months ended June 30, here's how the company performed in comparison to a year earlier:

- Group revenue increased 69% to $181.7 million.

- Earnings before interest, tax, depreciation and amortisation increased 5.7 times to $20.5 million.

- Net profit after tax came in at $8 million, compared to a loss of $1.8 million.

- Operating cashflow up to $23.7 million.

- Strong balance sheet, with no debt and net cash of $27.3 million.

- Outlook: Revenue is forecast to grow 15% to 20% and underlying EBITDA expected to be flat.

The driver of Netcomm Wireless' strong full year result was its Telecommunication Infrastructure Equipment and Industrial Internet of Things segment thanks to the expansion of key projects. As you can see below, this was complemented by an improved performance by its Consumer Broadband segment. The segment returned to growth as management initiatives to improve the business took effect.

CEO & managing director Ken Sheridan appeared to be pleased with the company's performance. He stated that: "Over the course of FY18 we generated material revenues in our Telecommunication Infrastructure Equipment and IIoT business. We continued to receive and deliver large DPU orders to nbn for its FTTC project and importantly our relationship was further strengthened with the agreement to supply Network Connection Devices [NCDs], providing the in-home link for connectivity."

However, its revenue growth is expected to slow and underlying EBITDA is expected to be flat in FY 2019, which may have sent investors to the exits today. Management has advised that FY 2019 will be a year of consolidation to ensure a sustainable platform is in place to drive the next step change in growth expected for FY 2020.

Revenue is forecast to grow 15% to 20%. This forecast growth is dampened due to a slower than expected rollout of the nbn FTTC project and a slower rollout of the AT&T Fixed Wireless project. However, management was quick to point out that this revenue has not been lost, but rather it is deferred to future periods.

Underlying EBITDA is expected to be at a similar level to FY 2018, with "revenue growth offset by lower margins as the sales mix changes from higher margin Australian DPU sales to lower margin NCD sales and higher near-term component costs are incurred due to global industry wide shortages."

Should you invest?

Based on Netcomm Wireless' earnings per share of 5.5 cents, its shares are now changing hands at 15x earnings. I think this is a reasonable price to pay for its shares given its outlook for a flat FY 2019 before returning to growth in FY 2020.

In light of this, I would class it as a buy alongside IT hardware distributor Dicker Data Ltd (ASX: DDR) and accounting software company Xero Limited (ASX: XRO).