Interest rates are on the way up. At least, that's the general view. And most are expecting the first increase to be later this year or early next.

But that's not exactly a consensus view. And whatever consensus there was, is weakening.

Cue respected economist, AMP Capital's Shane Oliver. I think it's fair to describe Oliver as a 'cautious optimist', and I've always found his views to be sober and balanced.

Writing on the AMP Capital site, Oliver says:

"The RBA should avoid calls to raise interest rates prematurely just to prepare households for higher global rates. Such a move would be Iike shooting yourself in the foot in order to practice going to the hospital

"Nor should the RBA mess with the inflation target that has served Australia well.

"We don't see it doing either and continue to see interest rates on hold out to 2020 at least and can't rule out the next move in rates being a cut."

Which is saying something. There are plenty of permabears and Negative Nevilles and Nancys out there. But Oliver isn't one of them. And I think I detect a softening in his optimism.

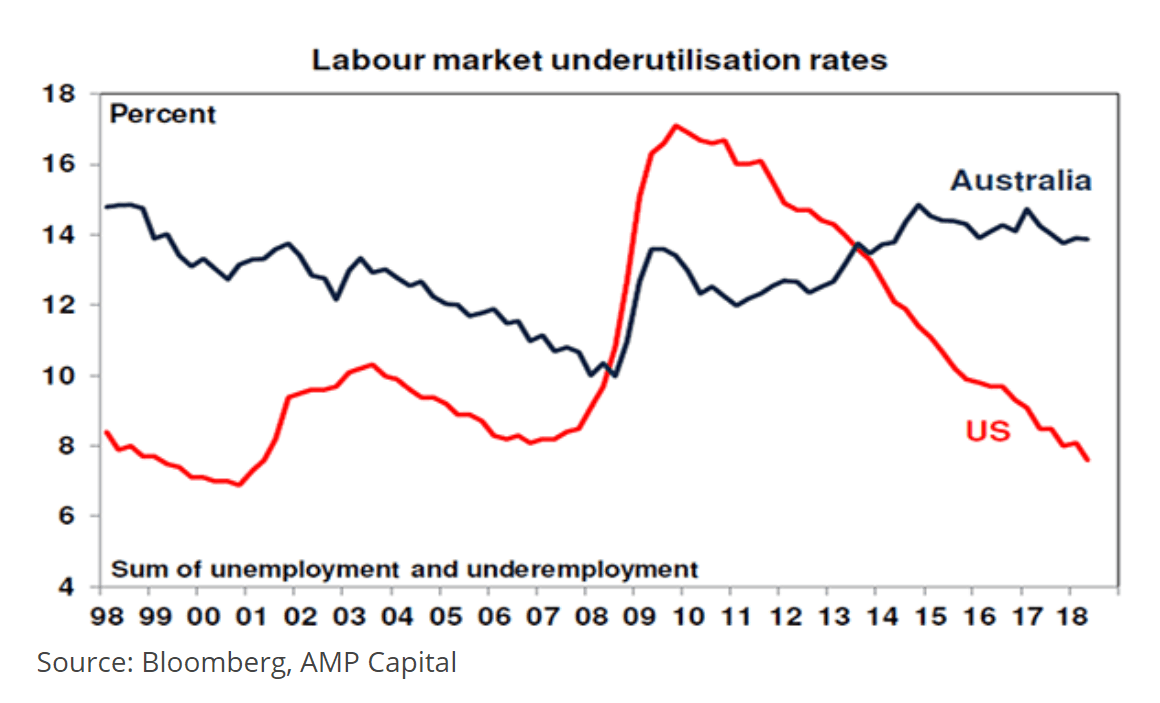

Here's one of the main culprits:

While US unemployment and underemployment falls, Oliver notes that Australia's remains stubbornly, essentially, unchanged.

According to Oliver:

"Raising rates when there is still high levels of labour market underutilisation, wages growth is weak and inflation is at the low end of the inflation target would just reinforce low inflation expectations"

Essentially, in my view, that's his call for waiting for more data to suggest that inflation is actually coming, rather than just on the assumption that overseas trends and forces will come to bear, here.

And, as I've written recently, the next rate rise (or two) that borrowers will pay are likely to come from the impact of rising overseas (essentially US) rates, which the RBA will surely know.

I remain a little more optimistic than Oliver. I think we'll see rates rise this year or next.

It won't change how I invest, of course, because 25 basis points is neither here nor there. But for indebted borrowers (or companies), rising rates will be a headwind that could seriously hurt those whose balance sheets are already stressed.