Last week's decision by the US Fed's new governor to lift the US central bank's cash rate to 1.75%-2%, while flagging the possibility of two more rate hikes in 2019 has put more pressure on the Australian dollar and helped lift the local share market at the end of last week.

The local dollar is now buying just US74.3 cents a little above a 52-week low and on an assessment of the fundamentals it looks more likely to go lower than higher over the 12-18 months ahead.

While the 24-hour news cycle leads to much attention over short-term drivers of foreign exchange rates the bigger picture is that nothing drives FX rates over the medium term other than yield differentials via the different rates central banks offer on cash and debt.

If we accept that, inter alia, local employment, CPI, housing, and industrial growth data will be insufficiently strong to allow Australia's Reserve Bank to lift rates until well until 2019 then its yield differential with the U.S. dollar will widen further.

In other words holding Australian dollars, or AUD denominated debt will be increasingly unattractive to institutional investors versus high-yielding US money market and longer-dated date assets, with lower demand equalling a lower Aussie dollar. Consider that the global bond market is on most estimates more than double the size of the global stock market and you can see how demand for currencies is greatly influenced by different rates on debt and cash.

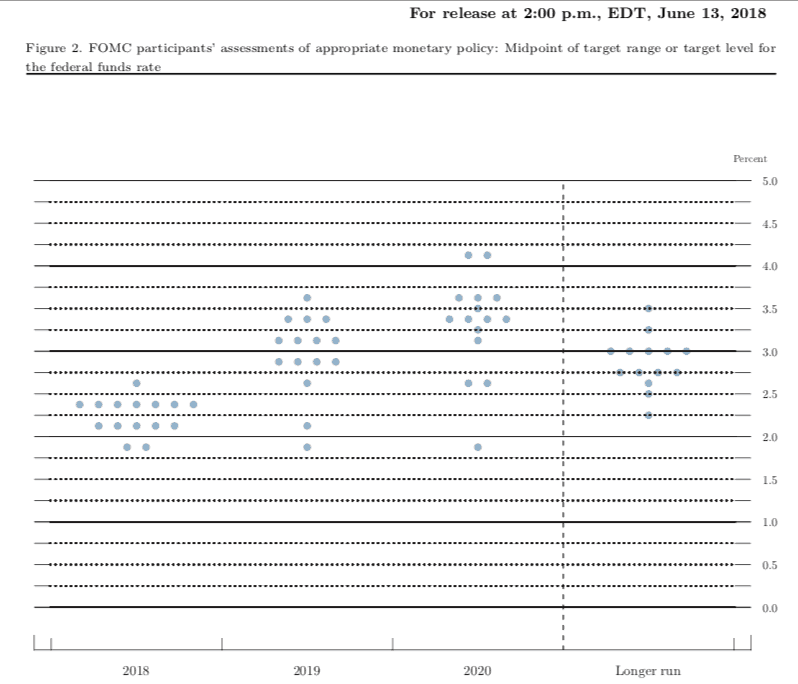

Not only does the average expectation of the US Fed's 15 members now mean two more rate hikes in 2018, but in 2019 more than half of the Fed's 15 members expect US rates to sit above 3%.

This is shown in the Fed's latest 'dot plot" chart below.

Source: US Federal Reserve

Of course this is no secret and forward expectations are priced into FX rates, although if the RBA is forced to delay rate hikes (or even cut rates again) on the back of falling house prices, soft wage growth, and inflation then the local dollar could fall lower over the 18 months ahead.

This scenario suggests businesses leveraged to the soft local economy are likely to underperform, while those leveraged to stronger U.S. growth and a weaker dollar may do well. Again, this is no big secret with US-dollar focused businesses like Altium Limited (ASX: ALU) and Computershare Limited (ASX: CPU) all hitting 52-week highs recently.

While the healthcare leaders like CSL Limited (ASX: CSL), ResMed Inc. (ASX: RMD) and Cochlear Ltd (ASX: COH) are all now sporting near record share prices and valuations.

Unfortunately, investing returns are always a function of price paid and as such the above businesses may not be the best way to play the weaker dollar theme, with CSL's strong growth perhaps making it still a buy.

If I wanted to make a riskier bet I would take Nanosonics Ltd (ASX: NAN) as a good quality medical device business with exposure to a stronger U.S. dollar, while fund managers like Janus Henderson Group (ASX: JHG) or Macquarie Group Ltd (ASX: MQG) still look ok value for anyone chasing U.S. dollar exposure.

The bottom line is that investors should consider business quality and value as the drivers of investment decisions before currency movements.

For example QBE Insurance Group Ltd (ASX: QBE) has strong leverage to rising US debt rates, yet shares recently touched multi-year lows as the business itself remains riddled with problems on the back of its overseas expansion. While packaging group Amcor Limited's (ASX: AMC) disappointing operating peformance has also seen its valuation slide lower even as the US dollar has headed higher.

Given the seemingly expensive valuations of Australia's leading US dollar earners, I'd again suggest investing directly overseas into leading U.S. companies to gain exposure to the growing U.S. economy. More so because valuations are still appealing relative to Australia's leading companies where some share prices are reflecting crowded trades.