Yesterday, Retail Food Group Limited (ASX: RFG) announced updated guidance to its expected full-year earnings.

The share price fell marginally, but I think that the market has overlooked the real substance and risk contained in the announcement.

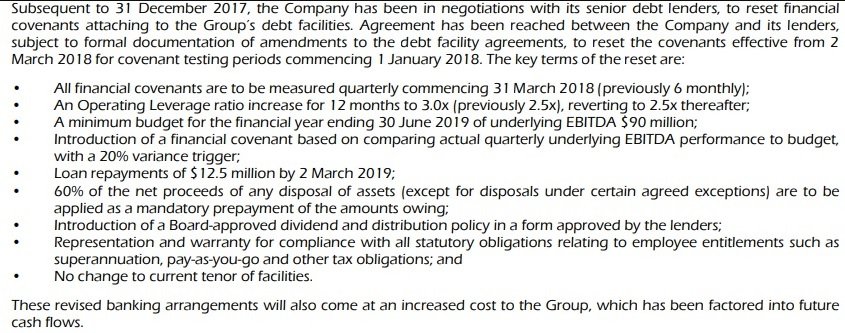

As we wrote a few months ago, Retail Food Group was bound by strict new banking covenants after the company revealed poor results for the half year to December 2017. It's worth sharing those covenants again here:

If RFG fails to maintain earnings before interest, tax, depreciation, and amortisation (EBITDA) of at least $90 million for the current full year, or if the quarterly EBITDA budget varies by more than 20%, it will trigger the debt covenants, which could require full repayment of debt on the spot.

RFG cannot repay all of its debt in one go, so the company is currently attempting to trade its way out of trouble, with the support of its bankers.

This is why yesterday's downgrade is a major concern. In 2017, RFG earned $123.5 million in EBITDA, and $75.7 million in Underlying NPAT.

Underlying NPAT yesterday was estimated to be $34.5 million for the full year in 2018 – a 55% decline. I would expect a similar decline in EBITDA.

If 2018 EBITDA falls by more than 30%, it will be below the covenant requirements of $90 million, which may cause the banks to take action to recover their loans.

This is a big problem because RFG simply cannot meet repayments of the whole loan currently. It will be forced to sell assets (burning the furniture to heat one's home) or raise capital. The company will struggle to raise capital in my opinion as shareholders will be unlikely to want to tip more money into a business that appears on the edge of the abyss.

Another concern is management's commentary about the weak retail environment and the uncertainty over whether $3 million in international licensing fees would occur.

Retail Food Group does not appear to have substantively eased the burden on franchisees or restructured its agreements with them, so the business model could still be as weak as it allegedly was at the time of media articles about the abusive franchise sector.

As a result, and given yesterday's profit guidance, my best guess is that Retail Food Group is either currently in breach or will very shortly be in breach of banking covenants.

Management stated that the company continues to maintain dialogue with their bankers, and it is possible that the banking syndicate will relax their restrictions to continue to permit the company room to trade its way out of trouble.

However, I would not rely on the generosity of bankers, and, while Retail Food Group might look "cheap" at 4x earnings, I would avoid it entirely. Given that the alternatives of a large capital raising or asset sales are not appealing, I think that Retail Food Group is in a very tough position, and could well go bankrupt.