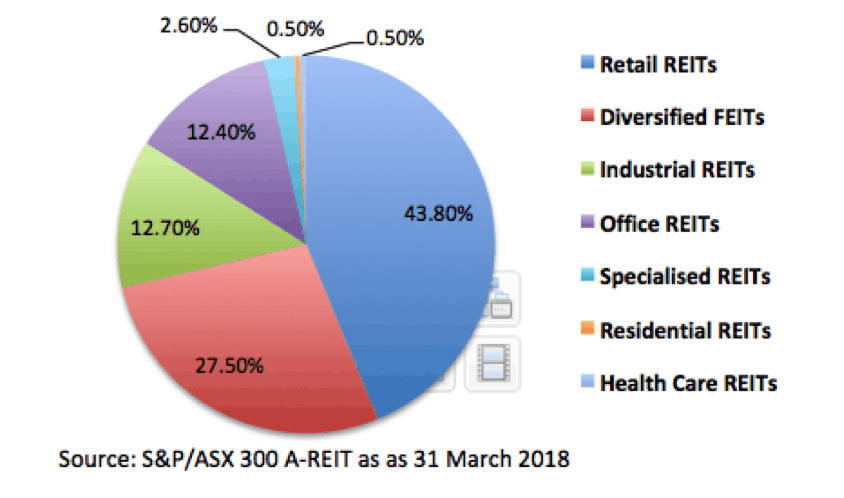

If investors that hold A-REITs (real estate investment trusts) believe they are exposed to the housing market, then they need to think again, as only 0.5% of the S&P/ASX 300 A-REIT (AUD) index is Residential Reits (See Figgure 1) including Mirvac Group (ASX: MRV) and Stockland Corporation Ltd (ASX: SGP).

Although, now it is positive not be exposed to housing via A-REITs with the softening residential housing markets.

Figure 1: S&P/ASX300 A-REIT sector breakdown

Figure 1: S&P/ASX300 A-REIT sector breakdown

The yields of A-REITs have been atrractive with the sector yielding an average of 5.5% pa (UBS calculation), which is generally unfranked as A-REITS pay distributions rather than dividends (for tax purposes as distributions are paid out of tax free income).

There is a strong negative correlation between the A-REIT sector's share price performance and changes in the long bond yield. Note that rising global rates have led to our long bond yields rising.

REITs are traditionally a defensive assest class, so rising rates have led some investors to rotate away into less defensive shares. But, the direct impact of rising interest rates on A-REITs' profits is more gradual as many of the A-REITs have investments in commerical real estate with long term contracts in place, which are linked to inflation (so can be a hedge to rising rates). A-REITs with higher gearing will feel the pain more from rising rates.

The A-REIT sector suffered signficantly during the GFC, with major falls on the back of what could be called mismanagment due to over-gearing, investment in non-related business, unsustainably high payout ratios and paying distributions from borrowings.

In the aftermath the sector has cleaned up its act but watch for A-REITS returning to bad habits by increasing gearing levels close to 50%, while the average gearing is around 29%, and paying out distributions from debt rather than earnings.

Investors will see the greatest benefits from A-REITS with low gearing, but A-REITS also offer secure distributions and attract institutional investors wanting exposure to institutional grade real estate.

The sector is likely to do better if interest rates remain low, while further softening in bond yields will negatively impact prices.

The six things to watch are:

- Gearing levels: Average gearing of 29%, moving towards 50% is in dangerous territory.

- Discount to net tangible assests (NTA): the long term average discount is 6.7% (UBS forecast), so watch for wider discounts suggesting there could be a buy-back, a takeover target or buying opportunity (See The Fool)

- Distribution yield: A-REITs trade on an average 5.5% distribution yield (UBS).

- Softening retail sector: Growing online purchases and dangerous levels of consumer debt seen as a negative for A-REITS heavily exposed to retail.

- Rising long bond yields: Will cause a sell off in A-REITS, especially those with more debt.

- Payout ratio: 100% or more means that no funds are being retained for growth.

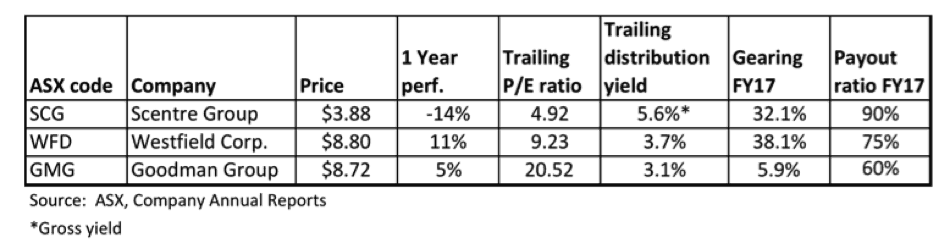

Figure 2 Top three A-REITS by market cap.