The de-rating among the big bank stocks from their tumbling share prices has put the sector at some of their most attractive valuations in years but bargain hunters should fight the temptation to jump in right at the moment.

I think there is a good chance that these stocks will face at least another profit downgrade later this year as analysts have not factored in the new risks that's being exposed by the Banking Royal Commission.

It is becoming increasingly obvious that the banks have been extending loans to people who cannot afford them and will likely have to increase safeguards to comply with responsible lending practices that lenders are obligated to follow.

This risk is not properly factored into the share prices of the big four that includes Commonwealth Bank of Australia (ASX: CBA), Westpac Banking Corp (ASX: WBC), National Australia Bank Ltd. (ASX: NAB) and Australia and New Zealand Banking Group (ASX: ANZ).

If anything, there could be some optimism creeping back into the sector with ANZ Bank issuing a report that the worst of the residential housing slowdown is behind us!

No conflict of interest there at all. Regardless, I think there's still a looming crunch time for the banks as tighter lending criteria and higher compliance costs will put considerable pressure on bank earnings.

Potential borrowers have been under declaring their living expenses and the banks have not been bothered to check on the accuracy of the information.

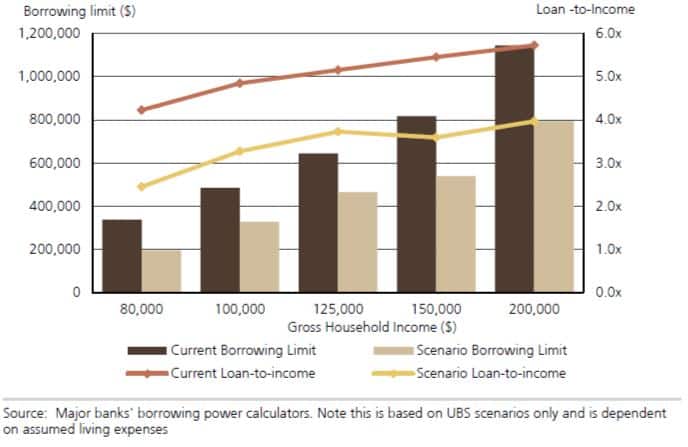

UBS has crunched the numbers to gauge the impact on the banks if they were to use a more reasonable level of assumed living expenses and the picture isn't pretty as consumers' ability to borrow could fall substantially.

This is particularly true for poorer households with the ability to borrow for a family on a combined income of $80,000 falling by 42%. This household had been able to borrow over $300,000 under the current system and that falls to about $200,000 if the bank assumes that their yearly living expenses is $50,000.

Downsizing: Impact on borrowing limits and loan-to-income ratios

I don't know about you, but $50,000 a year to support a couple of kids seems very realistic to me and would imply that I am enjoying few of life's luxuries.

The impact on wealthier households is not as dramatic but it's still very significant as the chart above show.

Given the strong correlation between mortgage and home values, I would be reluctant to believe that the worst of the housing slowdown is behind us – wage growth or not!

What's more pertinent to bank investors is that consensus earnings forecasts have not factored in this risk (let alone other risks uncovered by the Royal Commission, such as a potential class action). Analysts are tipping earnings growth for the big banks in FY19.

I can't help but feel there is downside risks to these projections.

If you are looking for earnings growth, you best look elsewhere. The good news is that the experts at the Motley Fool have picked their three top blue-chip stocks for 2018, which they think are best placed to outperform the S&P/ASX 200 (Index:^AXJO) (ASX:XJO).

Click on the free link below to find out what these stocks are.