In morning trade the Kogan.com Ltd (ASX: KGN) share price has surged 10% higher to $7.95 following the release of an outstanding half-year result.

For the six months ended December 31, Kogan delivered a 45.7% increase in revenue on the prior corresponding period to $209.6 million. Thanks to this strong revenue growth and a 1.4 percentage point lift in its gross margin to 19.4%, trading earnings before interest, tax, depreciation, and amortisation (EBITDA) came in 93.2% higher than the prior corresponding period at $14.1 million. In fact, this first-half trading EBITDA result was greater than the entire pro-forma EBITDA generated in FY 2017.

It was the same on the bottom line as well, with half-year trading net profit after tax (NPAT) rising 118.9% on the prior corresponding period to $8.1 million. This compares to full-year pro forma NPAT of $7.2 million in FY 2017.

On a diluted per share basis, half-year earnings were 9 cents. The board has elected to pay out approximately 77% of this as a dividend, with eligible shareholders due to receive a 6.9 cents per share fully franked interim dividend next month.

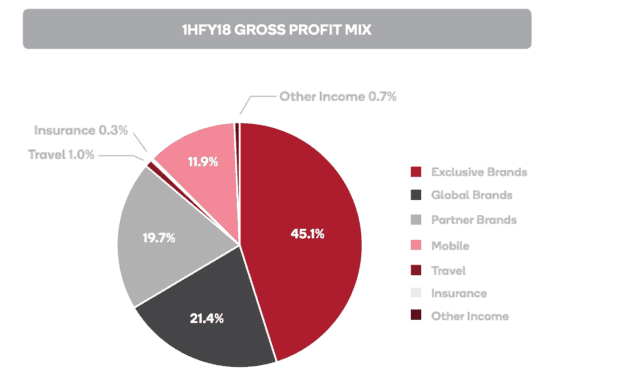

Management advised that the strong result was driven by growth across all product divisions, a 40.5% increase in active customers, and the expansion into new verticals. The Kogan Mobile segment, for example, delivered a 340.9% increase in revenue on the prior corresponding period. As you can see below, this the Kogan Mobile business now accounts for 11.9% of gross profit.

Whilst management once again reiterated that it will not be providing any formal EBITDA guidance for the full-year, it has stated its expectation that it will benefit in the second-half from further growth in its active customer base, Kogan Mobile, and the launch of insurance products and its internet offering.

Should you invest?

I've had a few doubts about whether Kogan would be able to live up to its valuation in the past, but I think this result has more than justified the incredible rise in its share price and the premium its shares trade at.

While it is still a high risk investment, I would put it up there with Lovisa Holdings Ltd (ASX: LOV) and Premier Investments Limited (ASX: PMV) as one of the best options in the retail sector today.