The numbers don't lie.

If you really want to beat the S&P/ASX 200 (Index: ^AXJO) (ASX: XJO) and grow your wealth, health care is the only way to go.

Yes, boring old health care.

According to Deloitte, health care spending is growing around 5% annually across Asia and Australasia and is estimated to top US$8.7 trillion dollars globally in 2020 – 10.5% of global GDP. It is mind blowing stuff.

On steroids

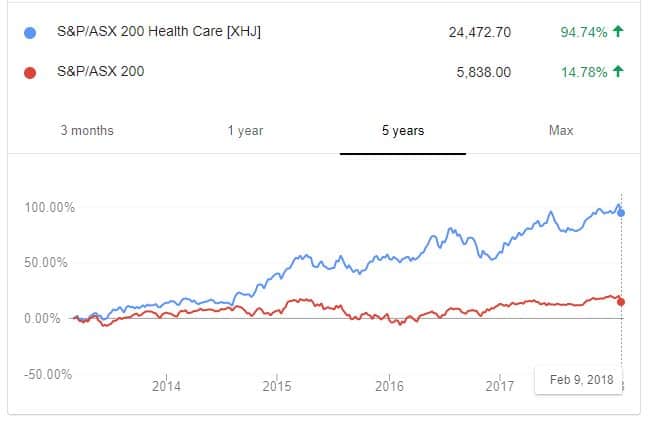

The cash is being funneled to major health care companies at a startling rate, juicing up investment returns. Just take a look at the below comparison of the S&P/ASX 200 to the S&P/ASX 200 Health Care Index (Index: ASX: XHJ):

Over the last five years the steroid injected S&P/ASX 200 Health Care Index has destroyed the returns of the S&P/ASX 200 by over 4x, led by big names like ResMed Inc. (CHESS) (ASX: RMD), Cochlear Limited (ASX: COH) and CSL Limited (ASX: CSL).

Too expensive?

There is a well-founded perception that health care companies are expensive. In a relative sense, when compared to the broad S&P/ASX 200 Index, this is certainly true.

The recent trailing price-to-earnings (P/E) ratio for the S&P/ASX 200 Health Care index is a huge 36.7 compared to just 18.5 for the S&P/ASX 200 Index.

Meanwhile, dividend yields for health care also trail at a stingy 1.6%, compared to 4% for the S&P/ASX 200.

This does not necessarily mean health care companies are overvalued. The industry is booming and unlike many sectors has a clear, sustainable growth outlook over the next decade. This is reflected in the projected forward P/E for the healthcare index which drops to 25.7.

According to the Australian Bureau of Statistics, 20% of Aussies will be 65 or older in 2040, from 15% in 2017, pushing one of the key markets for health care products far higher and accelerating the demand for health care locally.

This trend is similar for developed countries around the world. As people age, it is only natural that spending on quality of life should come ahead of discretionary spending, every time.

This supports the likelihood of continued above average earnings growth for companies in the industry which will naturally command above average share prices relative to earnings today. Though this also adds risk if individual companies fail to achieve expectations.

Low dividends allow reinvestment back into assets and research and development to ensure companies can keep up with growing demand and compound returns at high margins.

And boy, are margins high! CSL has an operating profit margin of 25.5% in 2017, while hearing device company Cochlear also produced operating margins of 25%.

A tick in every box

Still not convinced?

Health care stocks are not only growing at unparalleled rates and earning huge margins, but big companies like ResMed, CSL and Cochlear also have strong globally diversified earnings. This lowers geographic risk and can amplify returns from major currencies if there is a local downturn.

Health care remains an essential, defensive, growing, high margin industry. Individual companies are not infallible, but I think the industry makes it a formidable investment opportunity for smart investors.