Health insurers have recently been bid up to frothy multiples by the market. While some like NIB Holdings Limited (ASX: NHF) – a small insurer that has been rapidly claiming market share – deserve their day in the sun, Medibank Private Ltd (ASX: MPL) continues to puzzle me.

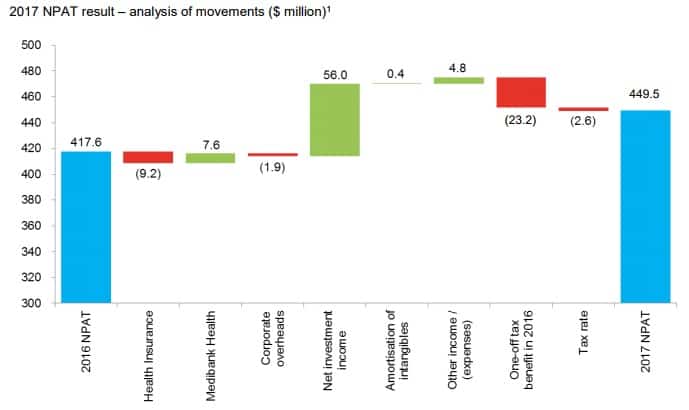

The Medibank share price has lifted around 16% this year after the company delivered 7.6% net profit growth at its annual report. However, I thought the company's results were mediocre, with the strong headline numbers masking several underlying problems:

- The health insurance business is still going backwards. The company lost 0.6% market share this year and health insurance profits fell an amount equivalent to ~2% of net profit after tax (NPAT).

- The lift in profits was almost entirely due to investment income. This year's investment income of $139 million reflects a 5.6% yield on Medibank's $2.5 billion portfolio – more than doubles last year's 2.4% yield.

- Medibank has revised its equity allocation downwards (taking less risk) and I'm doubtful the company can achieve a 5.6% yield in 2018 in a portfolio that is 80% bonds and cash.

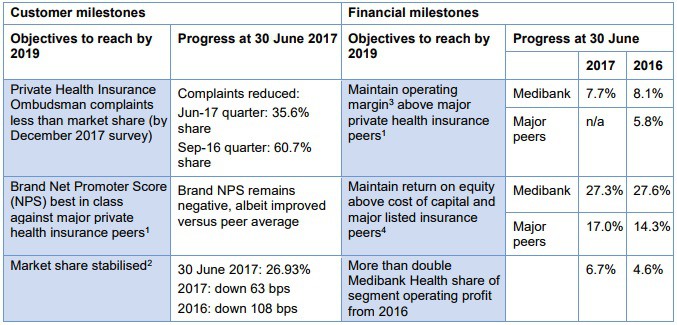

There were some surprise improvements, with a big lift in complementary services profit (now called Medibank Health) following divestments last year, and a huge reduction in complaints to the ombudsman. I give significant credit to management for their transparency.

I think there is a certain incoherence to some of the goals set above. For example Medibank may struggle to have a best-in-class Net Promoter Score (NPS; a reflection of how likely customers are to recommend the company's products), while simultaneously wanting to keep its margins and return on equity above those of peers.

This is because a higher NPS requires happier customers, and those usually require investment in customer service, product price, and the claims experience, which may also make it harder for Medibank to trim its claim expenses.

Likewise if the health insurance business is shrinking, and it is, it becomes much easier to double the Medibank Health share of operating profits.

On the topic of return on equity, Medibank generates more than 50% greater return than its peers do, for every dollar of equity in the business. That's usually suggestive of a solid competitive advantage.

However, can there really be a competitive advantage in a commoditised product like health insurance, especially if there are not-for-profit peers? There may be an advantage in scale and brand recognition, but if so Medibank's advantage is being eroded.

Should this stabilise for a few years, it would suggest to me that Medibank does have an advantage. If it doesn't stabilise, well…

I think Medibank is a good business with a good CEO, and were it more modestly priced I would be looking at it as a possible turnaround. However, I think it's currently priced in a way that suggests only modest returns for shareholders, with the possibility of further downside due to market share losses and thinner profit margins. As a result I continue to avoid it.