In the past few weeks since its latest quarterly report, I've sold virtually all my Yowie Group Ltd (ASX: YOW) shares. To understand why, I'll quickly revisit roughly why I bought them:

Why I bought Yowie:

I thought Yowie had a promising product, could be made at a decently profitable price, the ability to expand into related categories of movies, books etc, and it had a ~2-year period where it had the only capsules chocolate that could be sold in the USA. I believed that the books, animated shows and chocolate etc would all feed off each other to create a virtuous cycle, and that the 2-year grace period would allow the company to build a brand to fend off competition.

I held probably longer than I should, as my original forecasts when I bought suggested that Yowie would become cash flow positive in financial year 2018. Management's own forecasts aligned with this, and the company was still growing. However, the last two quarters show a sharp reversal and I think Yowie's time is up.

Why I've sold it:

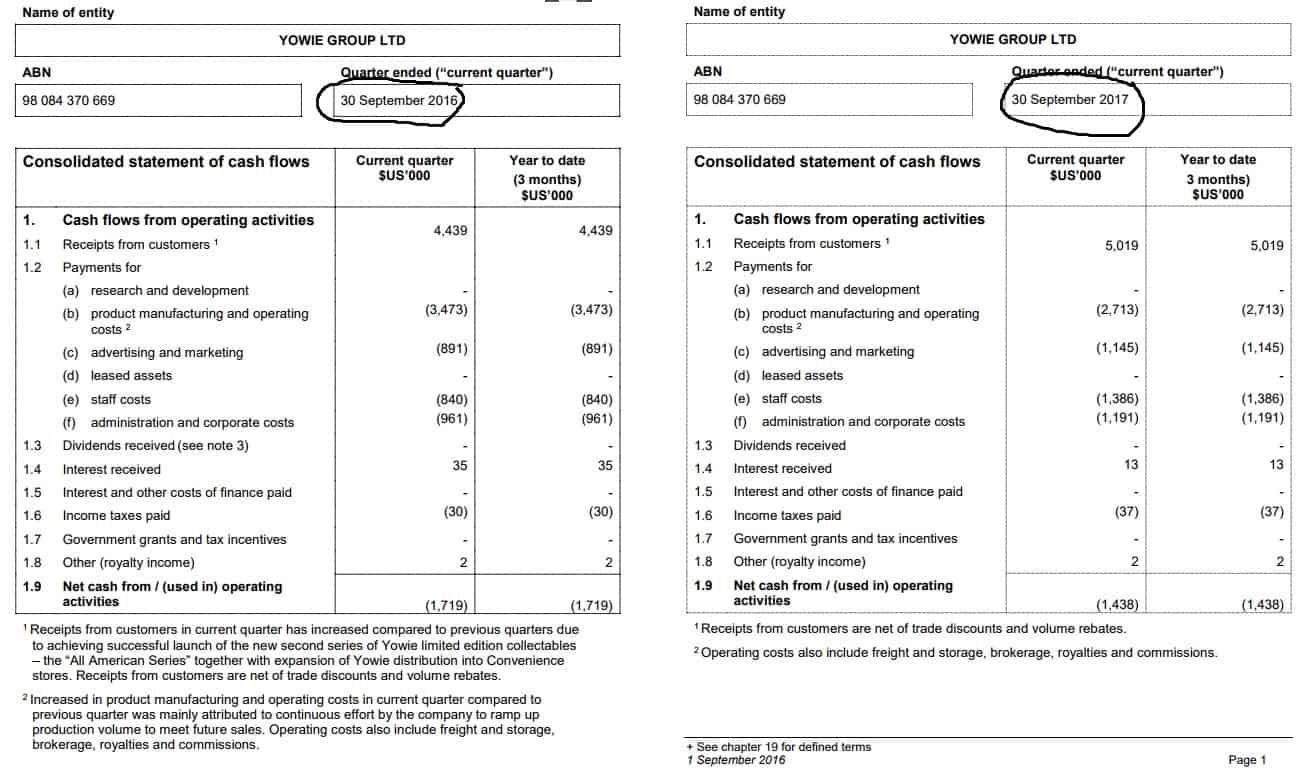

As part of its company development, Yowie saddled itself with a prohibitive cost structure to land globally experienced executives. From the most recent quarterly report, 27.6% of its sales were spent on staff expenses. 23.7% of sales spent on corporate costs. This means that 51.3% of the company's revenues last quarter went to staff and corporate overheads.

A further 77% of sales were spent on manufacturing and marketing. (This adds up to more than 100%, because Yowie is unprofitable). The real problem is that Yowie North America comparable sales collapsed 22% in the quarter. Sales fell primarily, I believe, due to strengthening competition as competing brands begin selling their capsule chocolates.

With a high cost structure and the heightened competition in its core market, I now doubt if Yowie will ever be profitable. The recent expansions into Canada and Australia are necessary to lift volumes but I believe that a) it is too early to tell if they will be successful and b) anecdotally the price point of the product appears wrong. Several anecdotes suggest the Canadian Yowies are selling for CAD$5 a unit which appears too high for the type of product that it is. Likely the cost of shipping to these locations plays a role, but more importantly I think competitors like Kinder Surprise could effectively undercut that price.

Additionally, if Yowie sales collapsed due to the introduction of competition in North America, it is hard to see the product becoming a huge winner in other markets where competitors are already entrenched. Total group sales were down 7% in the latest quarter and this follows a further 15% sales decline at Yowie's largest customer (Walmart) in the June quarter.

Management claims that Yowie is starting to see operating leverage, but I think this is inaccurate. The September 2016 quarter had higher relative cash outflows than September 2017, but this was due to inventory build for the following quarters. Advertising, corporate, and staff expenses were much lower in 2016 compared to 2017, and sales in that quarter were also juiced by a new Yowie Series release.

If anything I think Yowie is seeing operating deleveraging:

Compared to the prior corresponding period, sales are up 13%, manufacturing expenses are down 22%, although as noted this is due to inventory build in the prior quarter. Advertising is up 29%, staff costs are up 65% (!), corporate costs are up 24%. If you exclude the benefit of lower manufacturing expenses, Yowie went significantly backwards in the quarter. While it is myopic to just look at two quarters, with sales under pressure I do not see the company going anywhere in the near future.

This would be survivable if the company had a great product. However, management points out that sales this quarter were lower than what would be expected due to a delayed product launch. From my perspective, this is critical as it suggests that Yowies do not sell themselves, they need to be actively sold to people. This also suggests that the books and animated episodes etc are not enough to drive sales of Yowies, breaking a key point in my thesis.

Lastly, and I've critiqued this before, the company hasn't done a very good job justifying its strategy to shareholders. There has been a focus on social media influencing and such but the actual benefit to sales has not been demonstrated or quantified, in my opinion. Yowie has also been historically reluctant to share comparable growth figures or information about things like why it has hired consumer goods consultants to help it sell, when the company is already paying a high price for management's reputed expertise in this field.

In a nutshell, several core premises of my original thesis seem broken, and I do not believe that this is likely to change in the near future, so I sold almost all of my shares several weeks ago. I retain a tiny – and I mean truly insignificant – handful of shares so that I will follow the Yowie story for a while longer to see if my current analysis is borne out. I believe Yowie Group is not currently a worthwhile investment.