In 2006, Coles Myer divested the Myer business to a U.S. private equity group for $1.4 billion. After 3 years of ownership by private equity, Myer Holdings Ltd (ASX: MYR) was relisted in November 2009 at a float price of $4.10, giving the company a market capitalisation of around $2.4 billion.

A great piece of business for private equity, but in the ensuing years a disaster for long term Myer shareholders and holders from the IPO.

At today's prices of 73 cents, Myer only has a market capitalisation of around $604 million and has declined by 82% since its IPO. The stock has never actually traded above the $4.10 float price.

Earnings

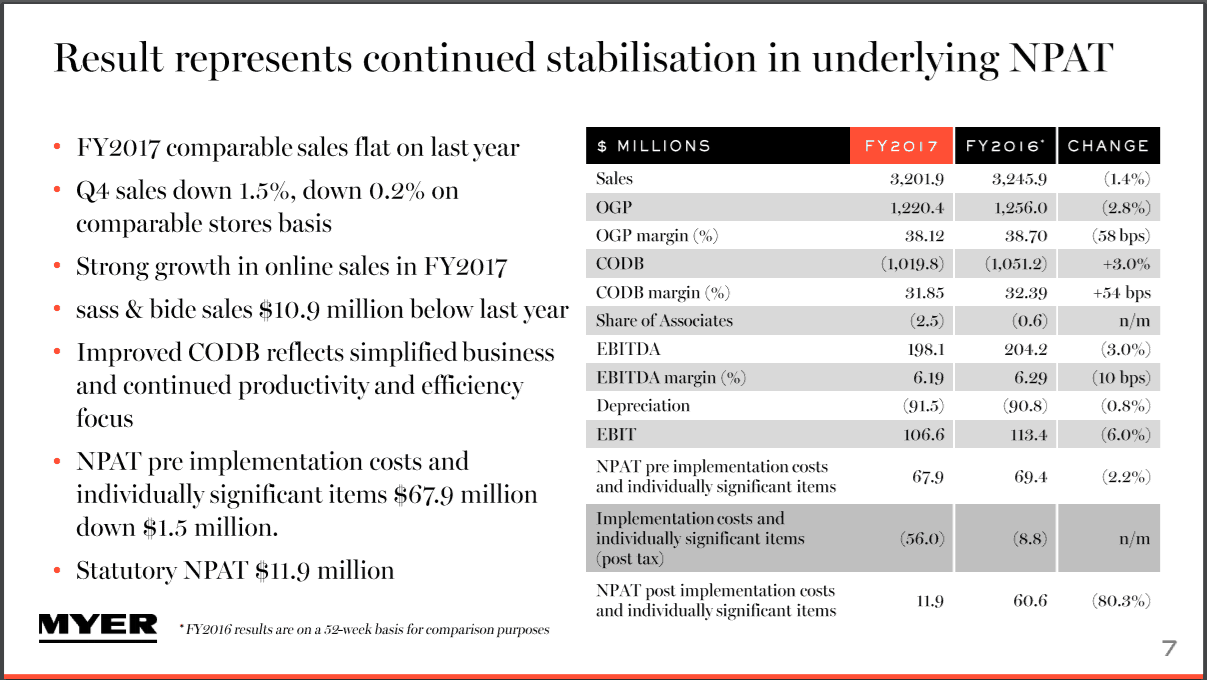

In September, Myer announced its results for the period ending July 29 2017. Sales were down by 1.4% at approximately $3.2 billion with margins also declining. EBIT was also down by 6% to $106.6 million and net profit (excluding the $56 million restructure) was at $68 million down 2.2%

Source: Myer FY 2017 Presentation

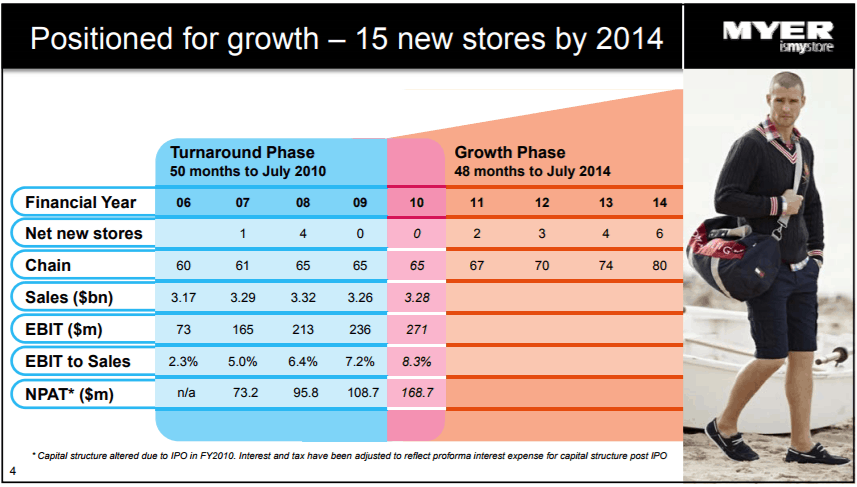

If you go back to Myer's presentation of its 2010 results you will find an interesting slide with its numbers going back all the way to 2006.

Despite Australia's population growing from 20.7 million in 2007 to around 24.6 million in 2017, Myer's sales have actually regressed, $3.29 billion versus $3.2 billion.

EBIT has also declined from $165 million to $106 million and NPAT has decreased from $73 million to $67 million. It's incredibly difficult to be upbeat on a business that has failed to progress and grow over a 10-year time frame.

Source: Myer FY 2010 Presentation

Myer's current store count is at 67 which is also well short of management's targets. With Myer stores at Belconnen, Hornsby and Colonnades also to be closed in the future it's going to be difficult for Myer to grow revenues without compromising margins as household wages remain sluggish and the Australian retail landscape's competitiveness increases with the Amazon introduction.

The pain for department store shareholders has not just been limited to Australia, as this week, Sears Canada announced it plans to close all of its remaining stores and lay off 12,000 employees. A once proud company now trades at 3.7c a share after being a $34 stock a decade ago.

Foolish takeaway

The high number of shorts who have been correct over the last few years can provide volatile price movements for swing traders especially when rumours of a takeover emerge.

However, for long term investors given the changing industry trends, store closures, flat to declining revenues, and newer entrants with superior business models, it's difficult to see a compelling long term investment case for Myer.

Myer's FY18 net profit forecast of $66 million is indicative of a business that is struggling to adapt. Morgan Stanley agrees and issued a price target of $0.60 cents last week, which remains the most bearish of analyst forecasts thus far.