If I had to pick one bank today, National Australia Bank Ltd. (ASX: NAB) shares would be at the top of my wishlist.

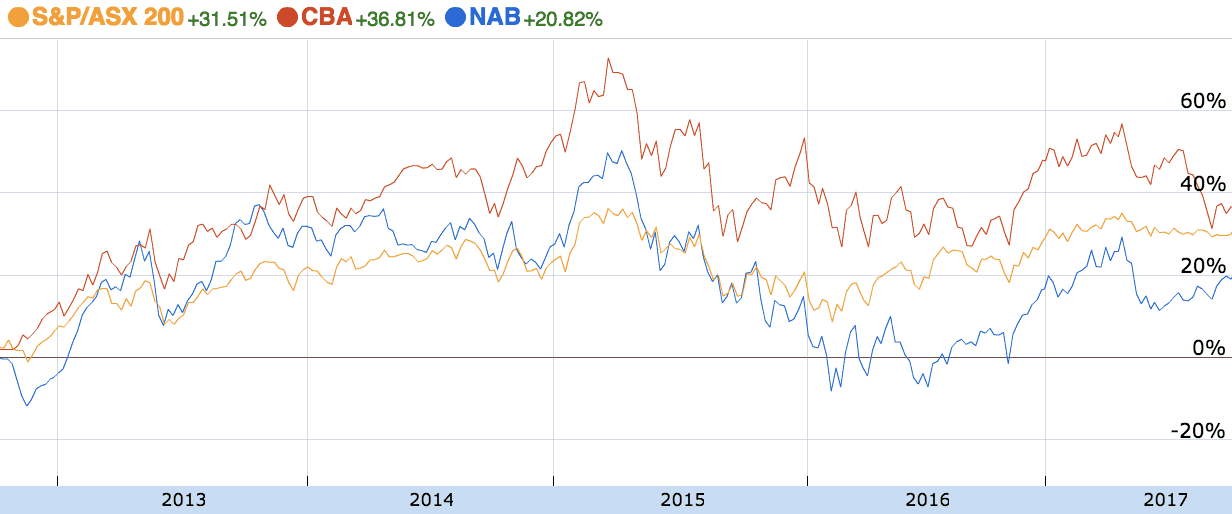

NAB share price over five years

As can be seen in the chart above, NAB's share price has underperformed the market, or S&P/ASX 200 (Index: ^AXJO) (ASX: XJO), and its key rival Commonwealth Bank of Australia (ASX: CBA) — before dividends — over five years.

Including its dividend payments — which are meaningful — NAB has returned a compound total return of 11.3% over the past five years, which is very close to the return of Commbank and more than the market.

Here are three reasons why I like NAB shares

- Dividends.

I'm not an 'income investor' per se but it's hard to go past NAB shares at a great source of dividend income. With its regulatory capital above reproach, I doubt NAB will have to cut its dividend payments to meet the regulator's standards. At today's prices, NAB shares are forecast to pay yearly dividends of more than 6% – plus franking.

- Earnings.

I think NAB has room to cut the fat (costs), invest in new technology, expand its market share and maintain its profit margins. That's more than can be said of some of its peers, in my opinion. If it maintains its dividend payments — or grows them modestly over time — NAB wouldn't need to achieve much profit growth to beat the market.

As an aside, if you flip a company's P/E ratio (NAB has a P/E of 13) upside down (E/P) you get the 'earnings yield'. That tells you the amount of profit, per dollar, investors expect a share to return in the future. NAB's earnings yield works out to be 7.5% or thereabouts. If you add NAB's dividend yield (6%) to that figure you get the total expected return: 13.5%. If that theory proves correct, NAB shares are expected to 'return' 13.5% per year.

Personally, I doubt the ASX 200 will be able to achieve that over the long term.

- Valuation.

NAB's valuation is the most compelling of the major banks, in my opinion. While I wouldn't go so far as to call it a 'bargain' I think it is around fair value.

Risks

NAB — like the other big banks — is just as risky as any other blue chip company listed on the stock exchange. The property and share markets could crash — that would be bad.

NAB could lose market share in business banking — that would hurt it, too.

Then, credit growth could enter a decade-long bear market. Given the meteoric rise in household debt levels over the past two decades something's got to give.

Finally, unemployment could rise and hit NAB even harder. That would hurt all of the banks, but you could expect NAB shares to be very volatile if we witness a spike in the unemployed population.

Foolish Takeaway

If I held more than 30% of my investments in investment property and bank shares I would not buy NAB shares. Nor would I buy NAB shares if I already held Aussie bank shares.

However, as an investor who owns European and US bank stocks, NAB would be the first local bank I buy.