The G8 Education Ltd (ASX:GEM) share price jumped 5% to $3.92 after the company released its half-year report to the market this morning. The company reported revenue growth of 2.1% to $368 million, while net profit after tax (NPAT) jumped 23% to $30 million. On an underlying basis, which includes refinancing fees and large currency gains last year, underlying NPAT was up 5% and underlying earnings per share fell 2% to 8.3 cents per share.

In this circumstance I believe it is more appropriate to focus on the underlying results, because of some big expenses last year that otherwise distort the results.

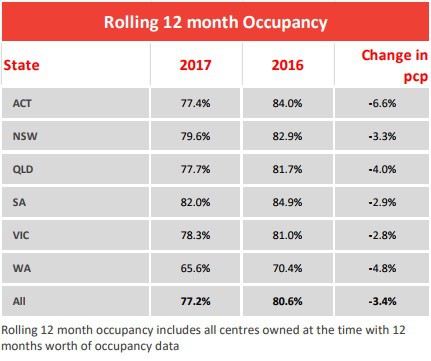

First half earnings grew at least in part because the company could save enough on wages and costs to offset increased rental expenses. Modest fee increases were unfortunately offset by weaker occupancy however, with 'like for like' (LFL) or 'same centre' occupancy falling 3.4% to 77.2%:

This is concerning as it comes at the same time as an increase in national supply, suggesting that G8 may not have a competitive advantage over other centres. G8 may have to increasingly compete on cost in the future, which could reduce its ability to grow fees and adjust for rising wages.

Fortunately, the company has taken steps to strengthen its balance sheet, and paid down some debt and announced a cut to the dividend. In Financial Year 2018 (FY18) which starts in January 2018 for G8, the company will switch to bi-annual instead of quarterly dividends. Instead of previous years' 24 cents in dividends, the company will pay 20 cents in 2018, and switch to paying between 70% and 80% of underlying profit from 2019 onwards.

Outlook

Management has confirmed that the outlook for company costs in the second half is in line with the first half. 8 new centres are to be acquired, with a possible impact on earnings of up to $3 million for the full year 2017. Full-year forecast of underlying earnings before interest and tax (EBIT) of 'mid-$170 million' are maintained. It's good to see G8 strengthening its balance sheet, but with business still declining and competition increasing, I continue to avoid the company at today's prices.