When Crown Resorts Ltd (ASX: CWN) reported its full year result earlier this month most of the focus was directed to the big fall in VIP turnover which was ugly, but not unexpected.

However, there was one point I think investors may have overlooked.

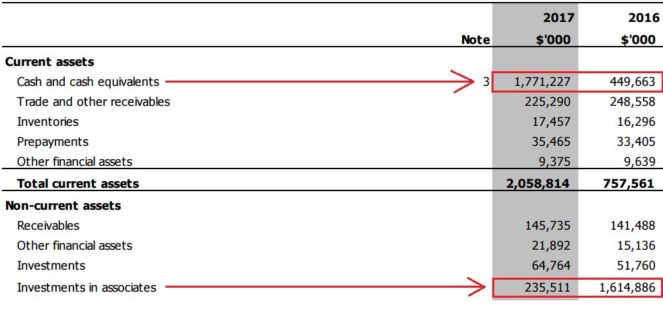

The company has built up a huge pile of cash! Cash and cash equivalents for the 12 months to 30 June 2017 more than tripled to $1.7 billion after Crown sold out of its investment in Macau's Melco joint venture. Today this cash pile makes up around 20% of Crown's $8 billion market capitalisation.

The sale is reflected on the balance sheet where we can see the shift in value from 'Investments in associates' and a corresponding increase in 'Cash and cash equivalents':

A company with a lot of cash can be a wonderful thing. Crown Resorts has three big plans for the cash to add value for investors:

1. Buy back shares

The company will buy back up to 29.3 million shares from investors. At today's share price that would use up around $341 million and reduce the number of outstanding shares by just over 4% leaving investors with a larger slice of future earnings.

2. Buy-back debt

The company will also resume buying back around $530 million of debt, a program it started earlier in the year. This will help to off-set the company's debt-to-equity ratio as it buys back shares.

3. Invest in growth

Finally, Crown Resorts will need cash on-hand to continue investing in Crown Sydney which is anticipated to require over $1.5 billion in capital expenditure over the next 3 years.

Should you buy?

Crown Resorts, like SKYCITY Entertainment Group Limited-Ord (ASX: SKC) and Star Entertainment Group Ltd (ASX: SGR), has been betting heavily on high value VIP business from China in the last five years.

Selling out of Macau tilts the strategy away from the Chinese market, but does raise the company's bet on inbound tourism demand and the health of the local economy.

If you're looking for international diversification, this new strategy won't meet your needs. However as I noted here, Crown will continue to pay an appealing dividend currently yielding over 5%.