The FlexiGroup Limited (ASX: FXL) share price fell 9% to $1.67 this morning after the company released its annual results for 2017. Here's what you need to know:

- Total income rose 17% to $462.8 million

- Net profit after tax (NPAT) rose 74% to $87.4 million

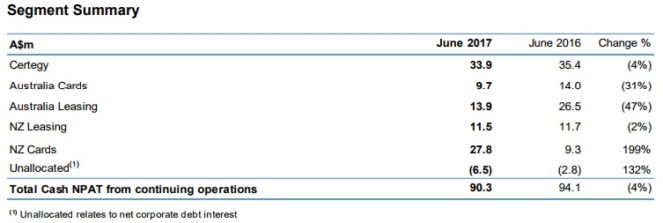

- Cash net profit after tax fell 4% to $90.3 million

- Earnings per share fell 11% to 24.2 cents

- Dividends per share fell 47% to 7.7 cents

- Gearing of 53%, down from 67% previously

- Outlook for significant growth in the Group's cards business

- Outlook for cash NPAT of $85 million to $90 million in 2018

- Outlook for Certegy business to return to growth in 2019

So what?

2017 was a weak year for FlexiGroup, with the acquisition of the Fisher & Paykel businesses offsetting a collapse in earnings from core businesses.

The decline in Australian cards and leasing segments was attributing to a combination of shifting receivables towards higher-quality, lower-margin commercial leases, plus a time lag in generating profits from the cards segment. The cost of funding interest free balances for new customers and an increase in losses drove card earnings lower.

Impairments and provision for doubtful debts were roughly in line with the previous year, after excluding some changes such as a one-off expense last year, and a full year contribution from NZ cards this year.

Now what?

FlexiGroup's guidance for 2018 of between $85 million and $90 million suggests that the business is expecting trading conditions to remain mixed, and profits could fall over the full year. However, investment in growth of approximately $30 million is expected to return the business to growth in 2019. FlexiGroup looks to be facing some near-term challenges, although management is very optimistic about the long term. Speaking for myself, I'm avoiding the company today.