I started buying shares of Berkshire Hathaway (NYSE: BRK-A) (NYSE: BRK-B) in 2005. It's been a wild ride ever since. I remember going to Berkshire's 2009 annual meeting in Omaha — a gathering of shareholders Buffett's skill has made rich over the years — and thinking to myself, "I'm probably the only one here who has lost money investing in Berkshire."

That probably wasn't true back then, but it's definitely not true today. Just read some of the headlines and opinions over the last week. "[Buffett's] track record since 2008 has not been very good," one analyst told CNBC. "Buffett is out of step," wrote The Wall Street Journal. "Berkshire keeps missing the mark," wrote another.

It's true in a way. Berkshire shares have been duds over the last decade, especially given the hype that comes with Buffett. Blogger Eddy Elfenbein noted yesterday that Berkshire has underperformed the Wilshire 5000 Total Return Index by almost 25% since 1998 — 14 years of underperformance. Shares have barely kept up with the S&P 500 over the last decade and have underperformed the index by 30% over the last three years. Among current members of the S&P 500, Berkshire's 10-year performance sits in 345th place.

You would have been better off investing in Treasuries over the last decade. Sorry, Warren — it's true.

What does that tell us? The standard answer is that Buffett has lost his touch. But that doesn't tell the whole story.

The CEO of any company has control over its operations, but not its share price. The company does business, earns profits, and reports to the public. It's up to the market to decide what shares are worth.

There's been a big divergence between internal results and share performance at Berkshire over the last decade. Buffett has done an excellent job managing Berkshire's assets in recent years. The market just hasn't rewarded him for it.

Think about this. Berkshire's shares have returned 4.7% a year since 2002. But net income per share more than double that during the period — 10% a year, or three percentage points a year faster than the S&P 500's earnings. Berkshire's book value grew 9.8% a year over the last decade. How many equity mutual funds performed as well? According to Morningstar, just 15 (out of more than 4,000). According to the EDHEC-Risk Institute, the average global macro hedge fund earned an annual return of 7.1% over the last decade, not including those that shut down due to poor returns. Buffett's investing performance over the last 10 years still makes him one of the best investors in the world. — easily.

And despite its size, think about some of the investments Berkshire made in just the last five years. It made deals in Goldman Sachs (NYSE: GS) , GE (NYSE: GE) , and Bank of America (NYSE: BAC) that loan sharks would envy. It spent US$36 billion buying Burlington Northern and US$9 billion on Lubrizol. Nearly US$86 billion has been plopped down on new investments over the last five years alone. For those worried that size would put a damper of Buffett's ability to make new investments, the verdict is clear: It hasn't.

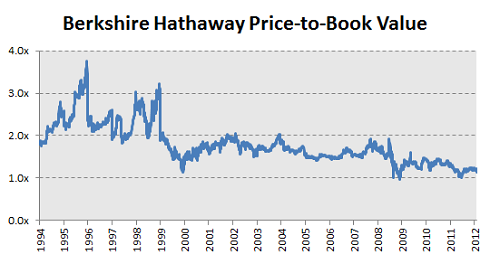

So what happened to shares? It's simple: valuations dropped. Berkshire's price-to-book ratio — arguably the best way to value the company — has fallen near the lowest level in at least two decades:

Source: S&P Capital IQ.

Part of this makes sense. Shares were probably overvalued in the 1990s, so recent poor performance may be more about a return to normalcy than a drop in confidence. Then there's Buffett's mortality. Shareholders will be lucky to have him managing Berkshire's portfolio for another decade. While vice-chairman Charlie Munger claimed on Friday that he's "never been more comfortable about succession or duration of culture than I am right now," investors may be totally justified to disagree. There will never be another Buffett, and valuations need to reflect it.

But given all that, what's a fair price for Berkshire shares today? There's no definitive answer, but several smart investors think it's somewhere between a lot and a whole lot higher than current prices.

Buffett himself is one of them. When he announced last fall that Berkshire was trading "demonstrably lower than intrinsic value" and began a rare buyback plan, shares traded for 1.09 times book value. They closed yesterday just a hair above that level — 1.14 times book value. "In my estimation the value is doing pretty well, and the price always catches up with it over time," said Markel chief investment officer Tom Gayner last Saturday.

Value investor Whitney Tilson gave a presentation last week arguing that Berkshire shares are now 33% below intrinsic value. Buffett's own response this weekend to a question about a common valuation technique called the "two-column" method suggests that his estimation of Berkshire's intrinsic value is around US$107 per class-B share, according to Motley Fool Inside Value advisor Joe Magyer. That's 30% above current prices.

So what's the market thinking? Buffett may have also explained that one this weekend: "The market is a psychotic drunk, and sometimes Mr. Market does very strange things."

If you're looking in the market for some high yielding ASX shares, look no further than "Secure Your Future with 3 Rock-Solid Dividend Stocks". In this free report, we've put together our best ideas for investors who are looking for solid companies with high dividends and good growth potential. Click here now to find out the names of our three favourite income ideas. But hurry – the report is free for only a limited time.

More reading

The Motley Fool's purpose is to help the world invest, better. Take Stock is The Motley Fool's free investing newsletter. Packed with stock ideas and investing advice, it is essential reading for anyone looking to build and grow their wealth in the years ahead. Click here now to request your free subscription, whilst it's still available. This article contains general investment advice only (under AFSL 400691).

A version of this article, written by Morgan Housel, originally appeared on fool.com